One Region, Six Rulebooks: A Business Guide to Stablecoin Compliance in Southeast Asia (2026)

Southeast Asia consistently leads global cryptocurrency adoption. According to the Chainalysis 2025 Global Crypto Adoption Index, Vietnam ranks #4 worldwide, Indonesia #7, and the Philippines #9, not driven by speculative trading, but by real-world utility. Remittances. Gig economy payouts. Currency hedging. These are financial survival tools, not investment products.

Yet for any stablecoin business trying to operate across this region, "Southeast Asia" as a compliance unit is a fiction. Six countries, six regulatory philosophies, six sets of operational requirements, and an enforcement environment that is tightening faster than most businesses have adapted.

What this guide covers:

- The regulatory status of stablecoins in each of the six major SEA markets as of mid-2026

- Vietnam's new pilot framework: what changed, what is still evolving, and what it means for foreign operators

- How the FATF Travel Rule is rolling out unevenly across the region and where the compliance gaps sit

- Data localization requirements in Vietnam and Indonesia and why they change the custody architecture decision

- What happens when a payment crosses multiple jurisdictions in the same flow

- A country-by-country comparison table plus a quick reference for the five smaller SEA markets

- Why compliance in this region ultimately starts with infrastructure, not legal review

For a deeper look at where each market sits in terms of stablecoin adoption before the regulatory detail, see: Stablecoin Adoption in Southeast Asia 2026.

What Makes Southeast Asia Unique for Stablecoin Businesses in 2026

Most global stablecoin discourse is framed around institutional finance: how banks tokenize assets, how treasuries optimize yield. Southeast Asia operates from a different starting point entirely.

Stablecoin adoption here is bottom-up. It emerged not because institutions needed a better settlement layer, but because millions of workers, freelancers, and small businesses needed something their local banking systems could not reliably provide: fast, cheap, stable value transfer.

Three structural forces drive this:

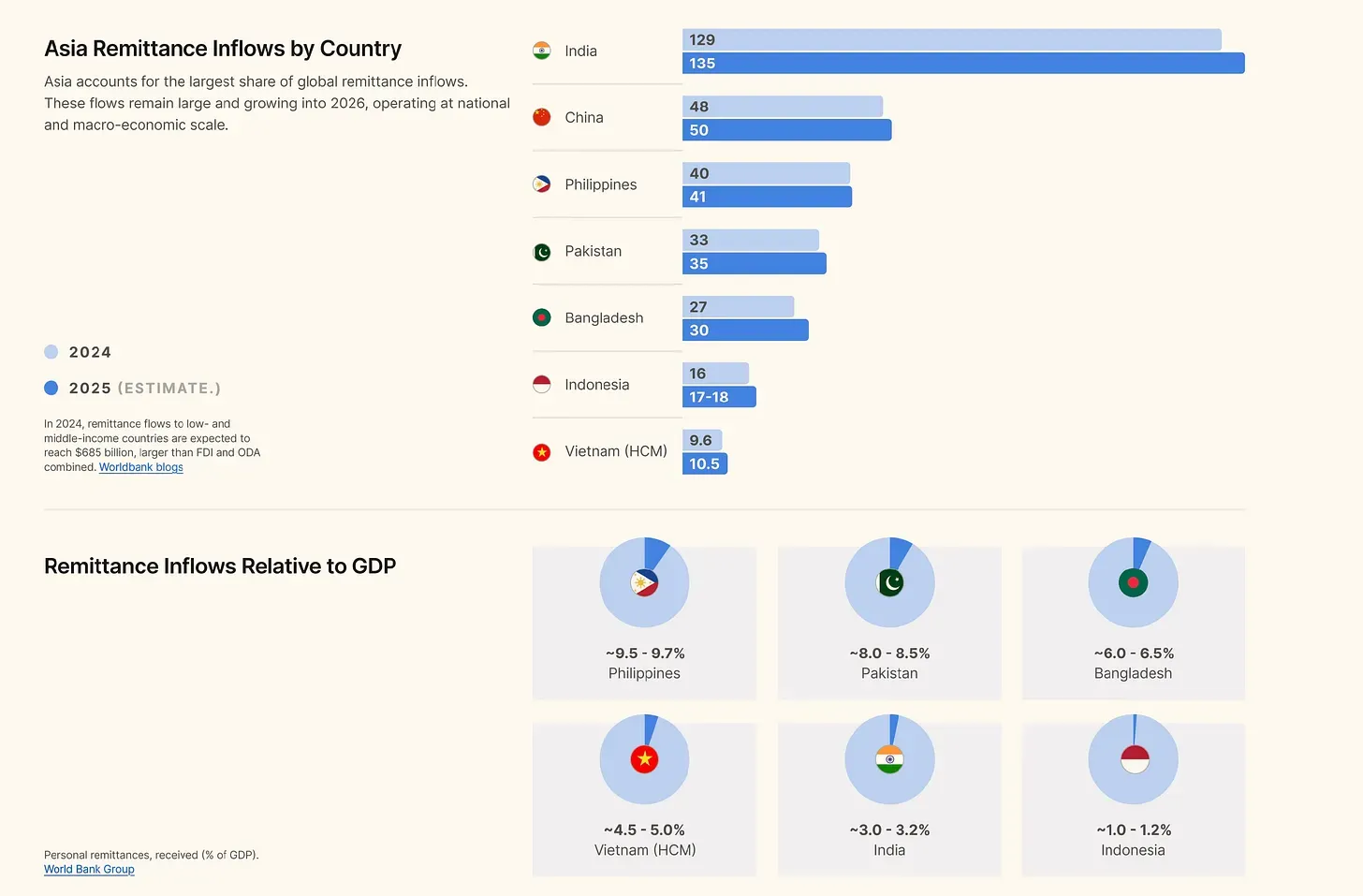

Remittance corridors. According to the Bangko Sentral ng Pilipinas, personal remittances from overseas Filipinos reached a record $39.62 billion in 2025. Sending money via SWIFT or Western Union costs 5–7% and takes 3–5 days. Stablecoins compress that to under 1.5% and near-instant settlement. This is not an edge case. It is the primary payment rail for millions of families.

Currency hedging. Indonesia's IDR and Vietnam's VND carry persistent volatility that makes USD stablecoins a rational default store of value. In Vietnam, P2P and OTC stablecoin premiums of 3–5% reflect genuine demand for USD access, not speculation. Freelancers, e-commerce operators, and SMEs hold USDT to preserve purchasing power.

Gig economy payouts. Developers, designers, and service providers across Vietnam, Indonesia, and Thailand increasingly invoice international clients in USDT or USDC, eliminating FX friction and SWIFT delays entirely.

The result: while the US and EU debate stablecoin innovation as a financial policy question, Southeast Asia has already resolved it as a practical one. Stablecoins are financial infrastructure: faster, cheaper, and more reliable than the traditional system for the use cases that matter most here.

This reality makes the regulatory question both urgent and complex. Regulators are not trying to stop a fringe technology. They are trying to govern a parallel financial system that is already deeply embedded in everyday economic life.

Vietnam: From Gray Zone to Controlled Pilot Market

Vietnam's regulatory transformation in 2026 is the most dramatic in the region. For years, crypto existed in legal ambiguity, neither fully legal nor explicitly prohibited, with millions of users trading almost entirely on offshore platforms. That waiting period ended.

Law No. 71/2025/QH15 on Digital Technology Industry, passed in June 2025 and effective January 1, 2026, formally recognizes digital assets and establishes the legal basis for a regulated crypto market. This is the foundational shift: cryptocurrency in Vietnam now has legal existence.

Decision No. 96/QĐ-BTC, issued by the Ministry of Finance on January 20, 2026, launched the pilot implementation of a regulated crypto-asset trading market. The licensing regime is among the world's most restrictive:

- Minimum charter capital: VND 10 trillion (~$400 million), exceeding commercial bank requirements in many countries

- 65% of capital must come from domestic Vietnamese institutions (banks, securities firms, insurance companies, tech firms)

- Foreign ownership capped at 49%

The pilot requires all transaction processing to occur through locally registered entities: a structural form of data localization.

Circular No. 32/2026/TT-BTC establishes the first comprehensive crypto tax framework: VAT exemption on digital asset trading, 20% corporate income tax on domestic organization profits, and a 0.1% transaction tax on individual investors and foreign entities.

On stablecoins specifically: Resolution 05/2025/NQ-CP explicitly prohibits the issuance of crypto assets backed by fiat currencies or traditional securities. The treatment of foreign-issued stablecoins such as USDT and USDC on licensed platforms remains an evolving regulatory question. Businesses should not assume a blanket usage ban, but should monitor Ministry of Finance guidance closely as the pilot develops through Q3 2026.

What this means for foreign operators (as of June 2026): Vietnam's vietnam cryptocurrency regulation 2026 framework makes direct market entry close to impossible as a standalone foreign entity. A foreign company cannot operate directly. It must be part of a Vietnamese-incorporated entity, take a minority stake (capped at 49%), and cannot control the licensed CASP. The practical options break down as follows:

| Entry Approach | Key Barrier | Practical Advice |

|---|---|---|

| Direct license application | Near-impossible: $400M capital + domestic ownership rules | Not viable for foreign startups or solo foreign operators |

| Joint venture with local partner | Must find a strong local partner (bank, securities firm, large tech); share control | Most viable path: provide tech, custody infrastructure, or capital as minority partner |

| Indirect (offshore service) | High risk as Vietnam tightens restrictions on offshore platforms | Usable for remittance/gig economy corridors but monitor regulatory direction closely |

| Focus on stablecoin utility without issuance | Still a gray area for payment use cases | Collaborate with local licensed entities for hedging and remittance corridors |

Vietnam wants domestic control and domestic capital. The demand side is enormous. For a company building stablecoin or custody infrastructure, the most realistic model is to partner with a local licensed entity rather than pursue a direct license. Indonesia operates under similar logic: both markets require local entity structures, local ownership floors, and local data infrastructure. Neither market is hostile to foreign expertise. They are hostile to foreign control.

Singapore: The Most Mature Stablecoin Framework

Singapore sits at the opposite end of the spectrum. The Monetary Authority of Singapore (MAS) has built the region's clearest, most permissive framework for stablecoin operators who meet its standards.

Under the Payment Services Act and MAS's stablecoin-specific framework, single-currency stablecoins pegged to the Singapore Dollar or G10 currencies are regulated with explicit requirements around reserve backing, redemption at par, and capital adequacy. This creates genuine legal certainty.

The FATF Travel Rule is fully enforced. Singapore has committed to CARF information exchange by 2028. SGD-pegged stablecoins account for over 70% of non-USD stablecoin volume in the region.

For businesses building multi-jurisdiction stablecoin operations, Singapore functions as the natural regional headquarters and compliance hub, highest certainty, clearest licensing pathway, best correspondent banking access.

Thailand, Sandbox-Driven Innovation

Thailand's Securities and Exchange Commission (SEC Thailand) governs digital assets with a regulatory sandbox approach that has allowed stablecoin pilots to advance in practical settings, notably in tourism and B2C payment contexts, before full legislation.

The sandbox framework gives operators room to test without full regulatory exposure, though it also means legal certainty remains limited compared to Singapore. Thailand has committed to CARF exchange by 2028. The Travel Rule framework is actively developing.

Thailand's approach rewards early engagement: operators who enter through the sandbox pathway build regulatory relationships that create durable market position when rules finalize.

Indonesia, Compliance at Scale

Indonesia presents both the largest population opportunity and the most operationally complex compliance environment. The Otoritas Jasa Keuangan (OJK) assumed oversight of crypto markets from Bappebti in 2025, signaling a shift toward more rigorous financial regulation.

Stablecoin usage is driven primarily by hedging against IDR depreciation and geographic fragmentation, 17,000 islands create structural barriers to traditional banking access that stablecoins bypass efficiently. Travel Rule enforcement is accelerating under OJK. Data residency expectations are tightening, tracking a trajectory toward localization requirements similar to Vietnam.

For stablecoin businesses, local entity structure and local data infrastructure are increasingly non-negotiable for operating at scale in Indonesia.

Philippines, Remittance-Led Stablecoin Growth

The Bangko Sentral ng Pilipinas (BSP) licenses Virtual Asset Service Providers under a framework shaped heavily by the country's FATF greylisting history. This means robust AML/CFT requirements are built into VASP licensing from the start.

Stablecoin adoption in the Philippines is predominantly remittance-driven, the OFW corridor represents $39.62 billion in annual personal remittances per BSP 2025 data. BSP's approach is practical: license compliant operators, enforce AML, support innovation that reduces remittance costs.

Neither the Philippines nor Vietnam have committed to CARF implementation yet. This creates a specific cross-border data gap: information flows that work smoothly between Singapore, Thailand, and Malaysia encounter friction when transactions involve Vietnamese or Filipino counterparties.

Malaysia, The Emerging Middle Ground

The Securities Commission Malaysia (SC) has established a clearer digital asset framework than most ASEAN peers, with crypto exchange licensing, AML requirements, and CARF commitment for 2028. Malaysia's approach is conservative but navigable, foreign operators can enter via SC licensing without the extreme capital thresholds Vietnam imposes.

Malaysia is increasingly positioning itself as a secondary regional hub for operators seeking ASEAN market access at lower cost than Singapore's structure requires.

Southeast Asia Stablecoin Compliance Comparison (2026)

| Country | Stablecoin Framework | Travel Rule Status | Data Localization | Foreign Operator Access |

|---|---|---|---|---|

| Vietnam | Pilot; fiat-backed issuance restricted | Developing | De facto (local entity + local processing required) | Restricted (49% cap; ~$400M capital) |

| Singapore | MAS-regulated; most advanced in region | Enforced | Permissive | Yes, with MAS license |

| Thailand | Sandbox-based | Developing | Moderate | Sandbox pathway |

| Indonesia | OJK oversight; tightening | Accelerating | Tightening | Restricted (local entity required) |

| Philippines | BSP VASP licensing; AML-heavy | Partial enforcement | Moderate | Yes, with BSP license |

| Malaysia | SC framework; CARF 2028 | Developing | Moderate | Yes, with SC license |

Sources: Chainalysis 2025, FATF, local regulators (2026). SEA stands out for the combination of high real-world adoption and complex orchestration requirements.

For a global framing of how these frameworks compare to MiCA and the US GENIUS Act, see: GENIUS Act vs. MiCA vs. Asia Sandboxes.

The FATF Travel Rule, Southeast Asia's Compliance Equalizer

Across Southeast Asia's regulatory patchwork, one requirement is becoming universal: the FATF Travel Rule.

The Financial Action Task Force's Recommendation 16 requires Virtual Asset Service Providers to collect, verify, and transmit originator and beneficiary information with every transfer, the data must "travel" with the transaction to enable tracing. According to Chainalysis's 2025 regulatory round-up, 85 of 117 jurisdictions globally have passed or are actively implementing Travel Rule legislation, up from 65 in 2024. In APAC specifically, 85% of financial hubs have already implemented the requirement.

The operational implications are significant:

- VASP-to-VASP transfers: Both sides must exchange verified counterparty data before settlement. This requires interoperable compliance protocols, and not all regional VASPs have implemented compatible systems.

- Unhosted wallet transfers: VASPs must collect originator and beneficiary information from their own customer, even when no counterparty VASP exists to receive the data.

- Threshold variations: FATF recommends a $1,000 minimum threshold, but individual jurisdictions set their own, meaning a single cross-border transaction chain may trigger different reporting requirements at each hop.

Vietnam and the Philippines have not yet committed to CARF, while Singapore, Thailand, and Malaysia are all targeting 2028 CARF implementation. This asymmetry creates specific operational friction in intra-regional corridors that businesses need to account for at the infrastructure level, not the legal review level.

Southeast Asia vs. Other Regions: Stablecoin Landscape 2026

| Criteria | Southeast Asia | Europe (MiCA) | Latin America |

|---|---|---|---|

| Primary adoption type | Grassroots + real utility (remittance, hedging, gig economy) | Institutional + rules-based | Inflation hedging + parallel finance |

| Regulatory character | Mosaic / fragmented (6 rulebooks) | Harmonized across EU | Fragmented but improving |

| Key stablecoin drivers | Remittance (PH), volatility hedge (ID, VN), tourism payments (TH) | Institutional settlement, tokenized assets | USD substitute, inflation protection |

| Adoption intensity | Very high (VN #4, ID #7, PH #9 globally, Chainalysis 2025) | Moderate | Very high (Brazil, Argentina) |

| Travel Rule | Uneven rollout; VN & PH not yet CARF | Strict EU-wide enforcement | Rolling out gradually |

| Data localization | Strong (VN, ID) | Not required | Moderate |

| Foreign operator access | Difficult in VN/ID; accessible in SG, MY | Easy (EU passporting) | Moderate to difficult |

| Stablecoin issuance | Restricted (VN bans fiat-backed issuance locally) | Clear framework (ART/EMT under MiCA) | Relatively open |

| Biggest risk | Regulatory fragmentation + policy flip | High compliance cost | Policy volatility + capital controls |

| Biggest opportunity | Orchestration moat + real-world usage at scale | Institutional treasury products | USDT/USDC volume growth |

Sources: Chainalysis 2025 Global Crypto Adoption Index, FATF, EY-Parthenon Stablecoin Survey, local regulators (2026).

The Hidden Layer Most Regulatory Analyses Miss

Most compliance guides stop here: a country-by-country matrix, a Travel Rule checklist, a licensing overview. What they miss is what happens when a single payment moves across these jurisdictions, which is exactly where the real compliance burden lives.

Consider a common payment flow in 2026:

Singapore → Vietnam → Indonesia → Philippines

At each leg, a different set of requirements fires:

- Singapore → Vietnam: Singapore enforces full Travel Rule; Vietnam's counterpart framework is still developing. The originator data Singapore sends may arrive at a Vietnamese VASP with no standardized protocol to receive or process it.

- Vietnam → Indonesia: Vietnam requires local processing through a domestically registered entity. Indonesia's OJK is tightening data residency. A business routing through both needs local entities in both, not a regional treasury account.

- Indonesia → Philippines: Both have active VASP frameworks, but neither has committed to CARF. Cross-border KYC data exchange relies on bilateral arrangements rather than a harmonized standard.

Each mismatch is not just a compliance friction, it is a potential transaction failure, a delayed settlement, or a regulatory exposure. The businesses that feel this most acutely are not edge cases: they are any fintech, payment operator, or neobank moving stablecoin value across two or more SEA markets at meaningful volume.

The problem is not that the rules are complex. The problem is that the rules are complex at the seams, at exactly the points where a transaction crosses from one jurisdiction to another. And most infrastructure was not built with those seams in mind.

Why Cross-Border Compliance Is Ultimately a Custody Problem

The cumulative effect of data localization, Travel Rule asymmetry, and local processing requirements points to a conclusion that legal analysis alone cannot solve: where you store your keys, and how your signing infrastructure is designed, determines what compliance is even possible.

Three requirements converge:

- Key residency for data localization. Vietnam's pilot requires all transaction processing through locally registered entities. Indonesia's OJK is moving in the same direction. When a stablecoin business operates across these markets, where private keys physically reside becomes a compliance question. A cloud-custodied solution where key material resides offshore creates immediate regulatory exposure in both Vietnam and Indonesia. Self-hosted custody infrastructure, where keys are deployed on the operator's own servers within the relevant jurisdiction, directly addresses this. This is also where Singapore-domiciled cloud custody and Vietnam/Indonesia-compliant self-hosted custody diverge architecturally. The choice is not a preference, it is dictated by each market's localization requirements.

- Travel Rule automation at the signing layer. Manual VASP-to-VASP data exchange does not scale at transaction volume. The Travel Rule requires counterparty verification and data transmission to happen at signing time, meaning compliance logic must be embedded in the approval workflow, not bolted on afterward. MPC-based custody systems enable this by integrating policy engines directly into the signing process: a transaction can only complete when required counterparty data is verified and, where applicable, transmitted.

- Multi-layer approval for cross-border treasury. Operating across six jurisdictions means different authorization requirements for different transaction types and different regulatory thresholds. Threshold signing via MPC, for example, requiring 2-of-3 key holders for transactions above a defined limit, enforces approval workflows at the cryptographic level, not the process level.

For a detailed breakdown of how MPC wallet architecture addresses these requirements in practice, see: What is an MPC Wallet? A Practical Overview for Startups and Institutions.

For businesses evaluating custody infrastructure for multi-jurisdiction SEA operations, the critical evaluation criteria are: self-hosted deployment capability (for Vietnam/Indonesia data localization), Travel Rule integration, programmable policy engine, and chain-agnostic signing. A direct infrastructure comparison is available at fystack.io/compare.

The Rest of Southeast Asia: A Quick Reference (June 2026)

The six markets above account for the overwhelming majority of stablecoin activity in the region. The remaining five countries present a different picture: limited regulatory development, small market sizes, or active restrictions that make them low-priority for most operators in the near term.

| Country | Stablecoin/Crypto Status | Insight for Foreign Operators |

|---|---|---|

| Brunei | Crypto is not legal tender; regulators issue high-risk warnings; no clear framework exists | Very limited opportunity; market is small and regulatory pathway is undefined |

| Cambodia | Legal with a license from the National Bank of Cambodia (Prakas 2024); banks and entities can offer crypto and stablecoin services including custody and trading, but unbacked crypto is restricted | More accessible than Vietnam or Indonesia if a license is obtained, but market size limits the opportunity |

| Laos | Heavily restricted: financial institutions are prohibited from participating; individual use is ambiguous | High risk, low activity; not recommended for near-term entry |

| Myanmar | Near-total ban on digital currencies in place since 2024-2025 | Not viable; political and regulatory risk is very high |

| Timor-Leste | Regulations are undeveloped; very limited information available | Market is extremely small with no meaningful stablecoin activity |

Fystack builds self-hosted custody infrastructure for fintech companies, payment operators, and neobanks operating across APAC and emerging markets. MPCIUM enables local key deployment, programmable approval workflows, and chain-agnostic signing for multi-jurisdiction stablecoin operations. Compare approaches →

FAQ: Stablecoin Compliance in Southeast Asia (2026)

Is USDT legal in Vietnam in 2026?

Vietnam's Law on Digital Technology Industry (Law No. 71/2025/QH15), effective January 1, 2026, formally recognizes digital assets. Resolution 05/2025 prohibits the issuance of fiat-backed stablecoins locally. USDT and USDC are not banned for holding or trading on licensed platforms: initial asset lists include stablecoins, but trading and settlement must be denominated in VND and foreign stablecoins cannot be used as a direct payment instrument. The broader regulatory treatment remains evolving. Businesses should monitor Ministry of Finance and Securities Commission guidance closely as the pilot develops through Q3 2026.

Can foreign stablecoin companies operate in Vietnam?

Not as a standalone entity. The licensed Crypto Asset Service Provider must be a Vietnamese-incorporated company. Foreign ownership is capped at 49%, at least 65% of capital must come from domestic Vietnamese institutions, and minimum charter capital is approximately $400 million. The realistic path for a foreign operator is a joint venture with a strong local partner such as a bank or securities firm, where the foreign side contributes technology, custody infrastructure, or capital as a minority stakeholder without direct operational control.

Which Southeast Asian country is most stablecoin-friendly for businesses?

Singapore offers the region's clearest and most mature framework. The Monetary Authority of Singapore regulates single-currency stablecoins with explicit standards, the Travel Rule is enforced, and licensing is accessible for qualified foreign operators. Malaysia is a viable secondary option for ASEAN access at lower cost.

What is the FATF Travel Rule and does it apply in Southeast Asia?

The FATF Travel Rule (Recommendation 16) requires VASPs to collect and transmit verified originator and beneficiary information with every virtual asset transfer. As of 2026, 85% of APAC financial hubs have implemented it. Singapore enforces it fully. Indonesia, Thailand, the Philippines, and Malaysia are at various implementation stages. Vietnam is developing its framework but has not yet committed to CARF. Non-compliance creates transaction friction, and increasingly, regulatory exposure.

How does custody infrastructure help with stablecoin compliance?

Self-hosted custody addresses two critical SEA-specific requirements: data localization (keys stored in-jurisdiction satisfy local processing requirements in Vietnam and Indonesia) and Travel Rule automation (policy engines built into MPC signing workflows enforce counterparty verification at the transaction level). Businesses operating across multiple SEA jurisdictions benefit from custody infrastructure that supports local deployment per market, programmable approval policies, and chain-agnostic signing for multi-chain stablecoin operations.