Visa vs. Mastercard: Buy vs. Partner in the Stablecoin Race - and What It Means for Lean Fintech Teams

Mastercard just spent $1.8 billion to own a piece of stablecoin infrastructure. Visa spent close to nothing and grew its stablecoin settlement volume roughly 50% in a single quarter anyway.

Same market. Same opportunity. Opposite playbooks.

TL;DR: Mastercard bought BVNK outright for up to $1.8B to own its stablecoin stack. Visa grew stablecoin settlement volume ~52% QoQ purely through partners, without owning any infrastructure. Neither approach is "correct." They reflect two different answers to the same build-vs-partner-vs-buy question every fintech adding stablecoin capability has to answer too, just at a smaller scale and with less room for error.

For a fintech founder deciding how to add stablecoin capability to their own product, that split is not a footnote, it's the whole decision. Buy the infrastructure, partner with someone who has it, or build it yourself. Visa and Mastercard just ran a live, well-funded experiment on the first two options. Here's what the data says, and what it means for teams operating at a very different scale.

The market right now

Stablecoins have stopped being a side conversation for the card networks. Three moves in recent months made that clear.

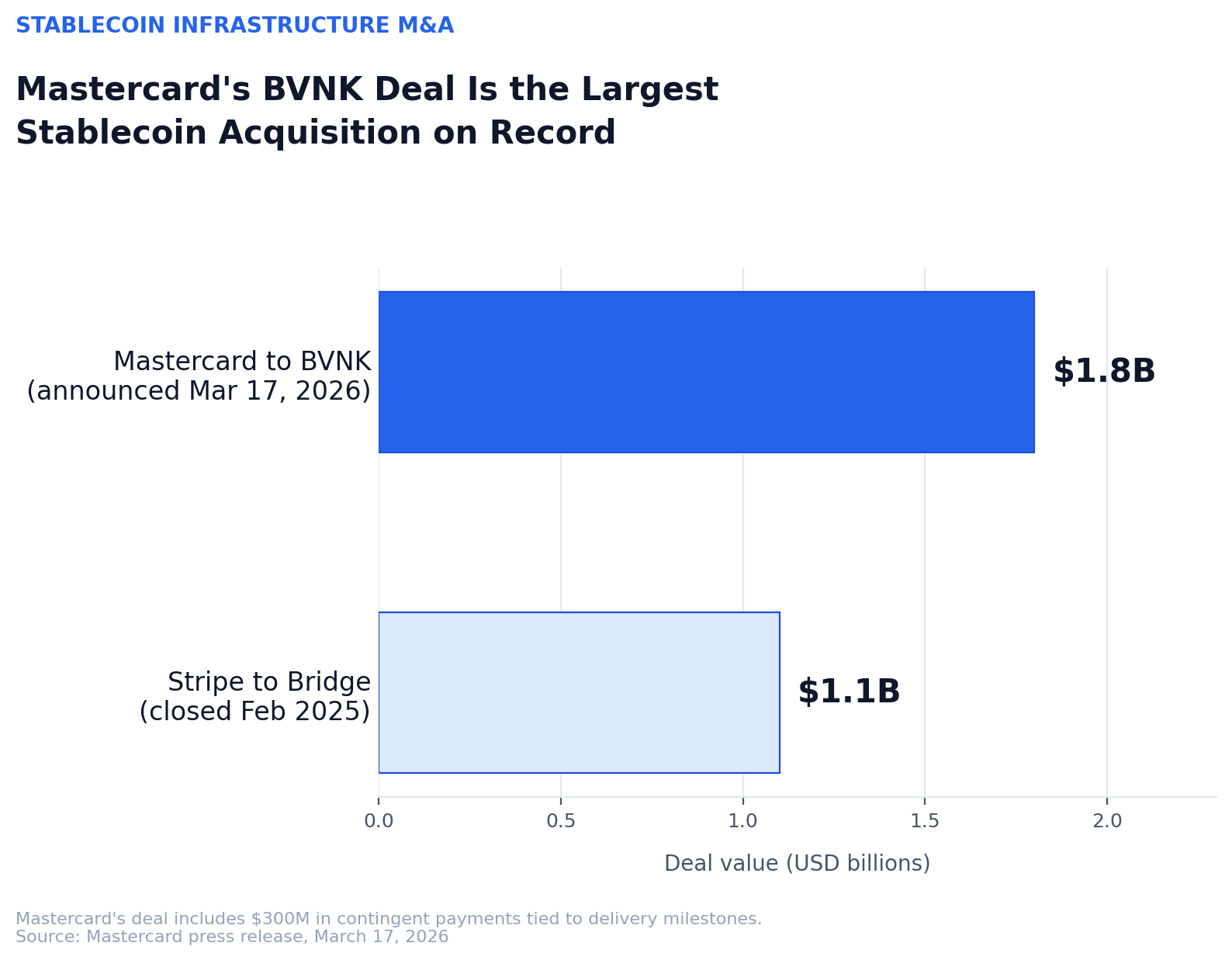

Mastercard bought BVNK. On March 17, 2026, Mastercard announced a definitive agreement to acquire BVNK, a B2B stablecoin infrastructure platform that had been processing more than $30 billion in annualized volume, for up to $1.8 billion, including $300 million in contingent payments tied to delivery milestones (Mastercard press release). It's the largest stablecoin-focused acquisition on record, ahead of Stripe's $1.1 billion purchase of Bridge in February 2025. The deal is still pending regulatory approval and is expected to close before the end of 2026.

Visa kept partnering instead of buying. Visa's stablecoin settlement run rate went from $4.6 billion annualized in FQ1 2026 to roughly $7 billion in FQ2, close to a 52% jump in one quarter, entirely through partners like Rain, Reap, and Bridge who own the rails and plug into Visa's network. Visa now runs 160+ stablecoin card programs globally without owning a single piece of stablecoin infrastructure directly.

Regulators are deciding who gets to play. On June 25, 2026, Japan's FSA approved Ripple's RLUSD as the first foreign stablecoin to clear its new equivalence test under the Payment Services Act, going live through SBI VC Trade the same day Nikkei reported Circle and Nomura are building a separate USDC-based settlement service targeting Japanese corporates in 2027. Brazil's central bank, meanwhile, is enforcing its own custody and FX rules on a hard October 30, 2026 deadline. Read our breakdowns of Japan's framework and Brazil's VASP requirements if you're building into either market.

Add it up and the signal is consistent: every major payments player now has a stablecoin strategy. What differs is how they're getting there.

Two strategies, one race

Mastercard is buying the stack. BVNK gives Mastercard direct control over issuance, settlement, and on-chain rails, the full plumbing, in-house. That's a bet that owning the infrastructure is worth the price tag, because it removes dependency on any third party's roadmap, pricing, or risk decisions. Mastercard's chief product officer framed the deal around chasing new addressable markets like remittances directly, not just defending card volume, and reportedly told investors that building similar capability internally would take considerable time.

Visa is renting the stack, at scale. Visa's approach treats stablecoins the way it treats every other payment method it doesn't issue: build the network, set the standards, let specialists compete to plug into it. The company isn't slower. Its stablecoin-linked volume is growing faster than Mastercard's acquisition can even integrate BVNK, but it's trading long-term control for near-term speed and lower capital risk. Visa's own stablecoin settlement run rate grew from $4.6 billion annualized in FQ1 2026 to roughly $7 billion in FQ2, close to a 52% jump in one quarter, entirely through partners like Rain, Reap, and Bridge who own the rails and plug into Visa's network. Visa now runs 160+ stablecoin card programs globally without owning a single piece of stablecoin infrastructure directly.

Neither approach is obviously "right." They're optimized for different constraints. Mastercard can absorb a $1.8 billion bet and a multi-year integration because its balance sheet and risk tolerance allow it. Visa can afford to let 160 partners compete because its core business is the network itself, not any single rail.

The part most industry commentary misses: this was never a volume race between stablecoins and card networks. It's a build-vs-partner-vs-buy decision, made twice, by two companies with almost identical market position and opposite answers. That's the more useful lesson for anyone smaller than either of them.

Which strategy fits a lean fintech team?

Most fintechs evaluating stablecoin infrastructure aren't choosing between a $1.8 billion acquisition and a global partner network. They're choosing between three realistic paths, each with a real cost.

Build in-house. Full control, no vendor dependency, no recurring platform fees. But you're now responsible for key management, multi-chain integrations, sanctions screening, audit trails, and every future compliance requirement in every market you touch, the same operational surface Mastercard just paid $1.8 billion to acquire pre-built. For a small team, this is rarely the first move. It's the move you make once you already know exactly what you need.

Partner with a rail provider. This is Visa's playbook, scaled down. You move fast, ship a stablecoin feature in weeks instead of quarters, and let a specialist absorb the compliance burden. The tradeoff is the one Visa itself manages at scale: your product now depends on someone else's uptime, someone else's licensing status in each jurisdiction, and someone else's decision about which chains and assets to support. If your provider loses a license in a market you serve, that's your outage.

Buy or license infrastructure you control. This is the middle path, and it's where most lean fintech teams building for APAC/MENA actually land: infrastructure that gives you the ownership properties of building in-house, your keys, your data, your compliance posture, without the multi-year engineering cost of building custody, signing, and chain integrations from zero.

The deciding factor isn't company size. It's how much of your custody and compliance posture you can afford to depend on someone else's roadmap. The table below is a rough guide, not a rulebook, for where a team is likely to land based on stage and market exposure:

| Team profile | Typical stage | Regulatory exposure | Likely fit |

|---|---|---|---|

| Pre-product / MVP, single market, low transaction value | Pre-seed to seed | Low (one light-touch jurisdiction) | Partner. Ship fast, validate demand, defer infrastructure investment |

| Live product, one or two regulated markets (e.g. Japan, Brazil, UAE), handling real client funds | Seed to Series A | Medium to high (custody segregation, audit trail requirements) | Buy/license infrastructure you control. Need demonstrable custody without a multi-year build |

| Multi-market APAC/MENA operator, exchange, neobank, or payment gateway with existing compliance team | Series A and beyond | High (multiple regulators, cross-border FX rules, VASP licensing) | Buy/license, moving toward in-house over time as volume justifies it |

| Category leader with balance sheet to absorb a multi-year build or acquisition | Growth stage / public | Very high, but well-resourced to manage it | Build or acquire. Mastercard's own playbook |

Most of Fystack's own customer base sits in the second and third rows: teams that are past the "just ship something" stage but nowhere near the point where a nine-figure acquisition makes sense.

The architecture lesson that doesn't change with strategy

Whichever path a team picks, one requirement shows up in every regulatory framework we've reviewed this year: custody has to be demonstrable, not just described.

Brazil's BCB Resolution 520 requires segregation between client and firm funds to be provable at the on-chain and key-management level. Accounting records alone don't satisfy the regulator. Japan's equivalence test for foreign stablecoins runs through four pillars, including audited reserve management and the technical capability to freeze transactions. Neither framework cares whether your stablecoin capability came from an acquisition, a partner integration, or in-house code. They care whether you can show your work.

That's the trap in the partner-only path: outsourcing the feature is fine. Outsourcing the evidence, the ability to prove, on demand, who controls which keys and where client funds actually sit, puts you one vendor incident away from a compliance problem that's legally yours, not theirs.

Where Fystack fits

Fystack's self-hosted custody infrastructure exists for the fintechs sitting in that middle path: teams that want the speed of not building from scratch, without handing over the one thing regulators actually ask for, demonstrable control over keys and client assets.

That means MPC-based key management you deploy and operate yourself, multi-chain wallet support built for the assets APAC and MENA regulators actually ask about, and an architecture designed to produce the audit evidence frameworks like Brazil's BCB resolutions or Japan's PSA equivalence test require, without a multi-year build.

If you're weighing build, partner, or buy for your own stablecoin roadmap, get in touch. We're happy to walk through where the tradeoffs actually land for your market and stage.

FAQ

Did Visa also acquire a stablecoin company, like Mastercard did with BVNK?

No. As of mid-2026, Visa has not made a comparable acquisition. It has expanded a multi-chain settlement pilot and grown volume through partners such as Rain, Reap, and Bridge, who own their own stablecoin infrastructure and plug into Visa's network.

Is Mastercard's BVNK deal already closed?

No. The deal was announced on March 17, 2026 and is expected to close before the end of 2026, subject to regulatory approval.

Does partnering with a stablecoin rail provider satisfy custody regulations like Brazil's or Japan's?

Partnering can satisfy the product requirement, but regulators generally hold the licensed or serving entity accountable for demonstrating custody controls, not just naming a vendor. Review the specific framework (see our Brazil and Japan breakdowns above) before assuming a partner integration covers your compliance obligation.