Japan Stablecoin Regulation Explained: What the 2026 Rules Mean for USDC, USDT, and Yen Stablecoins

TL;DR

- Japan's stablecoin regulation now creates a formal pathway for qualifying foreign stablecoins in Japan, effective June 1, 2026.

- USDC has a licensed distribution pathway via SBI VC Trade; USDT remains largely unavailable on licensed platforms.

- Japan is building a three-tier domestic yen stablecoin stack alongside opening to foreign instruments.

- In Japan, distribution is controlled by megabanks and licensed brokerages, not stablecoin issuers.

- Any operator handling foreign stablecoins in Japan is now inside the Payment Services Act regulatory perimeter, with mandatory client asset segregation.

- Fintechs serving Japanese clients need custody infrastructure that can handle both USD and local-currency stablecoins.

Glossary

Electronic Payment Instrument (EPI): Legal category under Japan's Payment Services Act for fiat-backed stablecoins. Issuance restricted to banks, trust companies, and registered funds transfer service providers.

Equivalence Standard: FSA requirement that foreign stablecoin issuers hold regulatory oversight broadly equivalent to Japan's own regime.

EPIESP (Electronic Payment Instrument Exchange Service Provider): License required to distribute stablecoins to Japanese users. SBI VC Trade is the primary current holder for foreign stablecoin distribution.

Progmat: Neutral blockchain rail for Japan's megabank stablecoin and tokenization programs.

Payment Innovation Project (PIP): FSA-approved framework for the megabank joint stablecoin PoC on Progmat, first granted to MUFG/SMBC/Mizuho in November 2025.

What Changed Under Japan's 2026 Stablecoin Regulation?

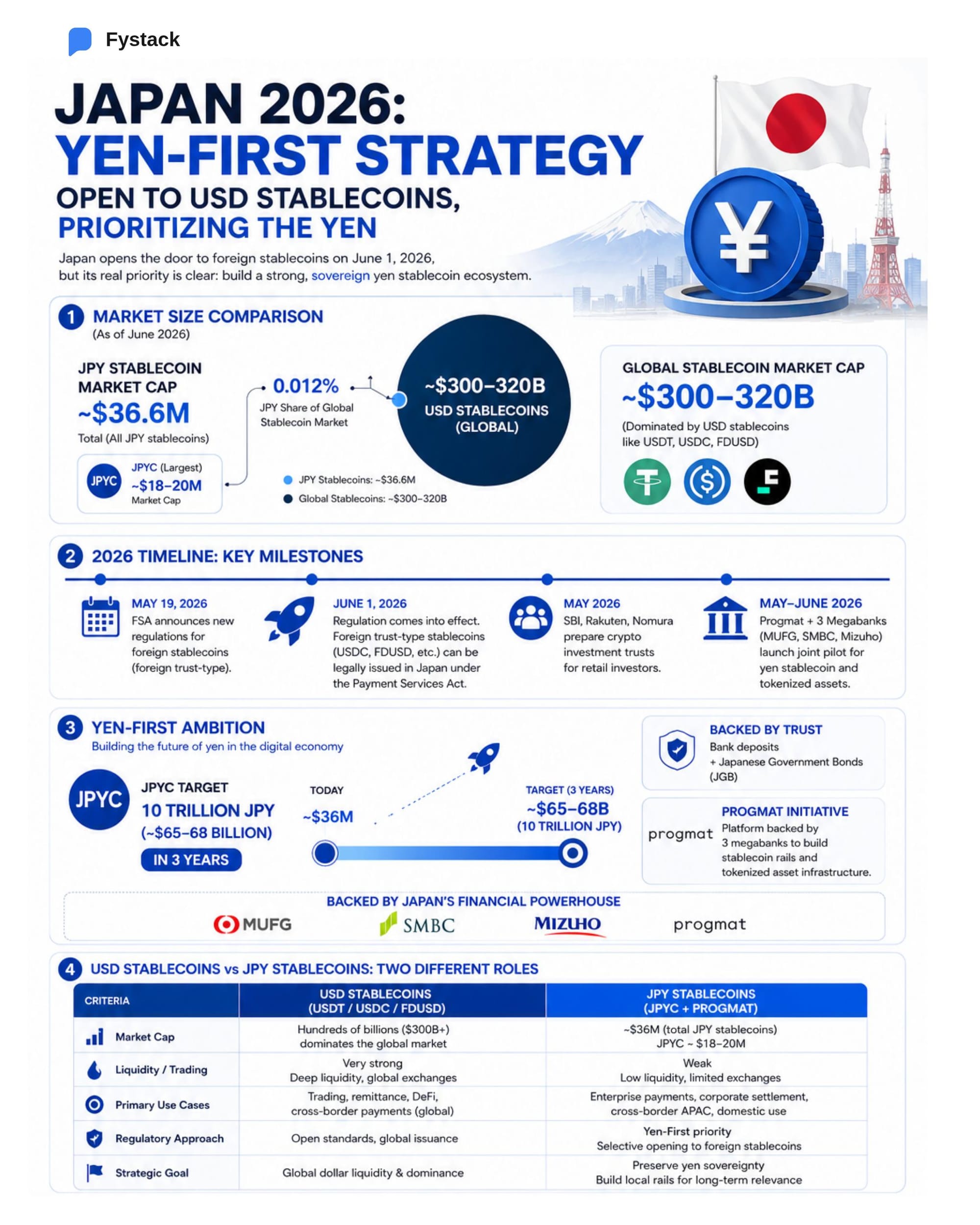

Japan's stablecoin regulation changed significantly in June 2026. Effective June 1, qualifying foreign stablecoins can now enter one of Asia's largest financial markets through licensed distribution channels under the updated Payment Services Act, governed by the Financial Services Agency (FSA).

Until this change, foreign stablecoins in Japan existed in a legal gray zone. Japanese exchanges historically avoided listing USD stablecoins such as USDC and USDT rather than navigate the compliance uncertainty. That blocked legitimate payment use cases and pushed cross-border flows through workarounds.

The updated framework resolves that. Foreign stablecoins in Japan can now operate through licensed Electronic Payment Instrument Exchange Service Providers (EPIESPs), provided the issuer meets the FSA's equivalence, reserve, and supervisory standards. USDC qualifies. USDT largely does not.

But the more important story runs in parallel: the FSA is also accelerating a domestic yen stablecoin architecture that may ultimately shape which payment flows foreign operators can access at all.

Japan Stablecoin Regulation at a Glance

| Topic | Summary |

|---|---|

| Foreign stablecoins | Allowed through licensed distributors (EPIESP) from June 1, 2026 |

| USDC | Eligible; distributed via SBI VC Trade |

| USDT | Not currently eligible; no licensed distribution pathway |

| Domestic yen stablecoins | JPYC (retail), JPYSC (institutional), Progmat/Project Pax (megabank B2B) |

| Key regulator | Financial Services Agency (FSA) |

| Governing legislation | Payment Services Act (amended 2023, updated 2025-2026) |

| Custody requirement | Client asset segregation mandatory for all EPIESP license holders. For CAESP (crypto asset exchanges), PSA additionally mandates ≥95% of user assets in cold wallets; equivalent ratios for EPIESPs are not explicitly codified but asset segregation standards apply. |

Japan Stablecoin Regulation Timeline

| Date | Event |

|---|---|

| June 2023 | Payment Services Act amended; stablecoin framework introduced |

| August 2025 | JPYC Inc. receives FSA Funds Transfer Service Provider license |

| October 2025 | JPYC launched as Japan's first regulated yen stablecoin under the new framework |

| November 2025 | Payment Innovation Project (PIP) status granted to MUFG/SMBC/Mizuho consortium |

| February-March 2026 | FSA public consultation on foreign stablecoin ordinance (16 responses) |

| February-March 2026 | SBI Holdings and Startale Group announce JPYSC, targeting Q2 2026 |

| March 5, 2026 | Progmat/Project Pax joint PoC goes live with MUFG, SMBC, Mizuho |

| May 19, 2026 | FSA finalizes foreign stablecoin ordinance |

| June 1, 2026 | Foreign trust-type stablecoins recognized as Electronic Payment Instruments |

How Large Is Japan's Stablecoin Market (JPY)?

| Metric | Estimate |

|---|---|

| Global stablecoin market cap | ~$300-320 billion |

| Estimated total JPY stablecoin market | ~$30-40 million |

| JPYC circulating supply (est. early 2026) | ~$17-20 million |

| USDT circulating supply | ~$183 billion |

The entire estimated JPY stablecoin market is less than 0.01% of global supply. The market remains small relative to USD stablecoins, which is precisely why enterprise B2B adoption matters more than retail speculation for yen stablecoin growth. JPYC completed two Series B closes totaling approximately ¥4.6 billion (~$30 million), backed by Metaplanet, Sumitomo Life Insurance, and Yokohama Capital, with the investor base dominated by corporate Japan rather than crypto-native funds.

What Japan's Stablecoin Regulation Really Means

Foreign stablecoins can now legally operate in Japan. But large Japanese enterprises may still prefer payment networks built around domestic yen stablecoins and bank-backed settlement rails.

For fintechs, the key implication is this: in Japan, distribution matters more than issuance.

The entities that control distribution in Japan are the megabanks and licensed brokerages, not the stablecoin issuers. Whether the stablecoin is yen or dollar, access to Japanese enterprise payment flows runs through SBI VC Trade, Mitsubishi UFJ Financial Group, SMBC, and Mizuho. That does not change under the new rules.

Foreign Stablecoins vs. Domestic Yen Stablecoins

Here is what most coverage of Japan's stablecoin regulation misses: the real competitive tension is not between foreign stablecoins and yen stablecoins.

It's between yen stablecoins and Japan's existing banking system.

Most Japanese enterprises already settle payments through MUFG, SMBC, or Mizuho. Convincing them to move to any stablecoin rail - whether USDC or JPYC - may be harder than competing with USD stablecoins directly. They have SWIFT. They have megabank relationships. They have yen-denominated settlement that, while slow and expensive, is embedded across procurement, treasury, and accounting workflows.

This is the adoption challenge JPYC, JPYSC, and Progmat are navigating. And it explains why the megabanks building domestic yen infrastructure are both its strongest advocates and the most likely reason adoption moves deliberately rather than fast.

USDC vs. USDT in Japan

| Factor | USDC | USDT |

|---|---|---|

| Licensed distribution pathway | Yes (SBI VC Trade) | No |

| Issuer | Circle Internet Group | Tether |

| EPI-eligible status | Yes, under FSA equivalence standard | Not currently eligible |

| Availability on licensed platforms | Yes | Limited |

| Reserve transparency | Monthly attestations | Quarterly disclosures |

| Japan regulatory status post-June 1 | Electronic Payment Instrument | Gray zone remains |

USDC's pathway was established through SBI VC Trade's registration as a licensed EPIESP and an explicit Circle Internet Group partnership. Tether's USDT faces a higher bar under the FSA's equivalence standard due to reserve structure and the absence of a licensed Japanese distribution partner. For fintechs building stablecoin infrastructure for Japan, USDC is the only viable foreign stablecoin with a defined regulatory pathway today.

Japan's Three-Tier Yen Stablecoin Stack

Japan's domestic stablecoin infrastructure operates across three licensed issuer tiers, each serving a different market segment:

| Layer | Product | Issuer | License | Use Case |

|---|---|---|---|---|

| Retail / Web3 | JPYC | JPYC Inc. | Type II Funds Transfer | SME payments, Web3; ¥1M/day cap per user |

| Institutional | JPYSC | SBI Shinsei Trust Bank | Type III EPI | Treasury, cross-border, enterprise; no daily cap |

| Megabank B2B | Project Pax / Progmat | MUFG, SMBC, Mizuho | Bank license | Corporate settlement, 300K+ clients |

JPYC transitioned from a prepaid payment instrument (operating since 2021) into a fully regulated stablecoin in October 2025 after JPYC Inc. secured an FSA Funds Transfer Service Provider license. Backed by yen deposits and Japanese Government Bonds. The ¥1M daily per-user cap limits enterprise use under the current license tier.

JPYSC (SBI Holdings + Startale Group, issued by SBI Shinsei Trust Bank) is Japan's first trust bank-backed yen stablecoin, targeting Q2 2026 and institutional use cases with no daily cap. This is the tier that could realistically compete with foreign stablecoins in Japan at enterprise scale.

Progmat (Project Pax) - MUFG, SMBC, and Mizuho launched a joint PoC in March 2026, targeting ¥1 trillion in B2B stablecoin issuance by 2028 across 300,000+ corporate clients. The ¥1T target, backed by existing megabank corporate relationships, is the more credible near-term benchmark for yen stablecoin growth at enterprise scale.

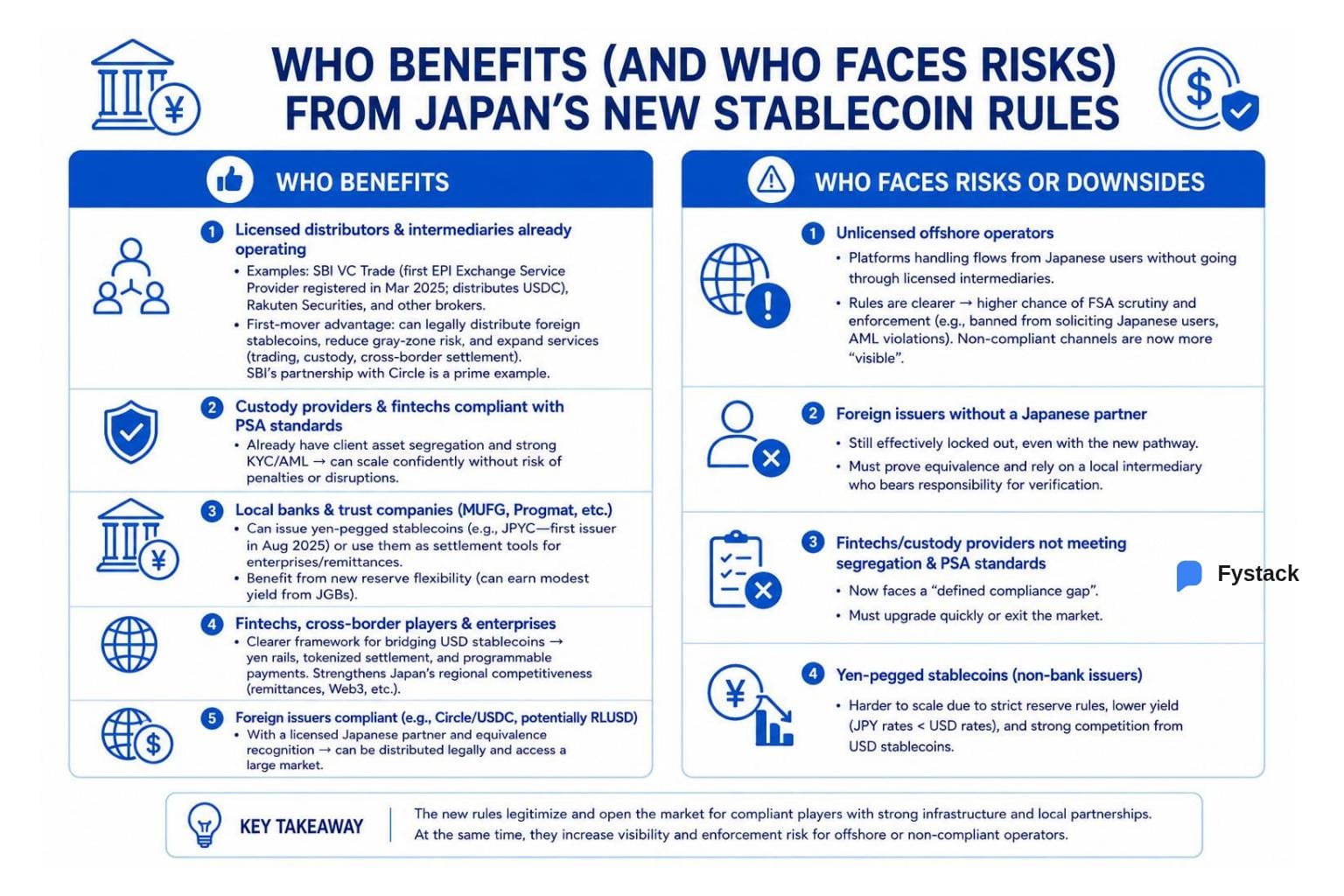

Who Benefits From Japan's New Stablecoin Rules?

Who benefits:

Licensed distributors already operating in Japan - SBI VC Trade, Rakuten Securities - have first-mover advantage on foreign stablecoin distribution. Custody providers whose infrastructure already meets Payment Services Act standards can serve a newly clarified market without gray-zone risk. Fintechs building cross-border settlement that bridges USD stablecoins to yen settlement layers now have a legal framework to operate within.

Who is at risk:

Unlicensed offshore operators handling Japanese user flows are more exposed, not less. The updated rules clarify the compliant pathway, which makes non-compliant channels more visible to regulators. Foreign stablecoin issuers without a Japanese-licensed distribution partner remain effectively locked out regardless of the new rules. Any fintech whose custody stack was not built for client asset segregation under Payment Services Act standards is operating in a defined compliance gap.

Custody Requirements Under Japan's Stablecoin Regulation

Five years ago, regulators worried primarily about whether stablecoins were fully backed. Under Japan's stablecoin regulation today, and analogous frameworks across APAC, the focus has shifted: regulators are increasingly focused on how businesses manage wallets, private keys, client asset segregation, and audit trails.

The FSA already mandates 100% reserve backing and redemption at par for all qualifying instruments. That risk is addressed at the issuance layer.

The live question for any operator handling foreign stablecoins in Japan post-June 1 is: how are you managing keys, segregating client assets, and demonstrating that to the FSA?

Key Management and Data Obligations Under Japan's PSA

Any Japanese operator handling foreign stablecoins is now definitively inside the Payment Services Act regulatory perimeter. The specific compliance obligations depend on license type:

- For CAESP (crypto asset exchange service providers), PSA mandates that at least 95% of user assets are held in offline cold wallets. Any assets held in hot wallets - up to the remaining 5% - must be matched by the operator's own assets (Redemption Guarantee Crypto Assets) held in a separate cold wallet. The operator absorbs hot wallet risk, not the user. Annual segregation audits by a certified public accountant or auditing firm are required.

- For EPIESP (stablecoin distributors such as SBI VC Trade), client asset segregation is mandatory under the same PSA framework. The explicit 95% cold wallet ratio applies directly to CAESP; equivalent ratios for EPIESPs are not codified identically, but the segregation and auditability standard is substantively similar.

Both license types are subject to Travel Rule obligations under the Act on Prevention of Transfer of Criminal Proceeds (APTCP): originator and beneficiary information must be collected and retained on all transfers, with transmission obligations applying when the counterparty jurisdiction has equivalent Travel Rule rules in force.

Notably absent from Japan's framework: there is no data localization requirement mandating that servers or private keys be physically located in Japan. The FSA's focus is on how assets are managed and segregated, not where infrastructure sits.

The same pattern is playing out across APAC. See Brazil VASP 2026 custody requirements, stablecoin infrastructure in Southeast Asia, and 2026 Crypto Compliance: Global Stablecoin Laws and Fintech Checklist.

Practical Roadmap for Fintechs Entering Japan

| Horizon | Action |

|---|---|

| Today | Use USDC via SBI VC Trade for Japan market access; confirm custody meets PSA client asset segregation standards |

| 12-24 months | Map payment stack against JPYSC (institutional flows) and Progmat/Project Pax (B2B settlement with Japanese corporates) |

| Long term | Build for multi-currency custody: USD stablecoins now, yen-denominated instruments as domestic rails mature through 2027-2028 |

Japan is not the last APAC market building domestic rails alongside opening to foreign instruments. Singapore, South Korea, and Hong Kong are moving in the same direction. Businesses that build multi-currency custody infrastructure now will not need to rebuild under regulatory pressure later.

How Fystack Helps Fintechs Operate in Japan

For most fintechs, the hardest part of operating under Japan's stablecoin regulation is not obtaining stablecoin liquidity. It's proving compliance around custody, asset segregation, and auditability to the FSA.

Any fintech handling foreign stablecoins in Japan post-June 1 is inside the Payment Services Act perimeter. Key management, client asset segregation, and audit compliance are mandatory. The same custody architecture will need to extend to yen-denominated instruments as domestic rails mature through 2027-2028.

Fystack's self-hosted custody infrastructure is built for multi-currency stablecoin environments under regulatory scrutiny. If you're building for Japan or any APAC market where the compliance bar on custody is rising, get in touch.

Frequently Asked Questions

What is Japan's stablecoin regulation?

Japan's stablecoin regulation is the framework under the Payment Services Act that governs the issuance and distribution of fiat-backed stablecoins in Japan. Established through a 2023 amendment and updated by FSA ordinances through 2026, the framework restricts issuance to licensed banks, trust companies, and registered funds transfer service providers. Distribution to Japanese users requires separate registration as an Electronic Payment Instrument Exchange Service Provider.

What changed in Japan's stablecoin regulation in June 2026?

Effective June 1, 2026, the FSA's updated Cabinet Office Ordinance formally allows qualifying foreign trust-type stablecoins to operate as Electronic Payment Instruments in Japan, resolving their previous gray-zone status under financial instruments law. Foreign stablecoin issuers must meet the FSA's equivalence standard to qualify.

How does Japan stablecoin regulation work?

Japan's stablecoin regulation requires issuers to maintain 100% reserve backing in qualifying assets (bank deposits, Japanese Government Bonds), guarantee redemption at par, and meet ongoing AML/CFT and reporting obligations. Foreign stablecoins must additionally meet an FSA equivalence standard proving their home regulatory regime is broadly equivalent to Japan's framework.

Can foreign stablecoins operate in Japan?

Yes, as of June 1, 2026, through a qualified pathway. Foreign trust-type stablecoins that meet the FSA's equivalence, reserve, and supervisory requirements are now recognized as Electronic Payment Instruments under the Payment Services Act. This is a curated opening with strict conditions, not a blanket approval.

What is the Payment Services Act?

Japan's Payment Services Act is the primary legislation governing digital payments, including stablecoins. Significantly amended in 2023 to create the stablecoin issuance framework, and updated through FSA ordinances in 2025-2026.

What is Progmat?

Progmat is a blockchain infrastructure platform originally incubated by Mitsubishi UFJ Financial Group (MUFG), now operating as a neutral industry utility. It is the shared rail for Japan's megabank stablecoin PoC (MUFG, SMBC, Mizuho) and the BlackRock Japan repo tokenization working group.