Stablecoins in Banking 2026: Neobanks vs Traditional Banks in the Race for Digital Settlement

Stablecoins are no longer a crypto experiment. They are becoming a settlement layer.

The biggest question in banking today is no longer:

“Should we experiment with digital assets?”

It is:

“Who will control digital settlement flows in 2026 - neobanks or traditional banks?”

Traditional banks are integrating tokenized deposits, real-time clearing infrastructure, and programmable settlement rails.

Neobanks, meanwhile, are embedding stablecoins directly into their product stack to bypass legacy payment networks.

The race is not about launching apps.

It is about owning the settlement layer.

And settlement ownership determines:

• Transaction volume

• Cross-border efficiency

• Liquidity velocity

• Regulatory leverage

Meanwhile, the window is compressing.

Institutions that take 24-36 months to modernize core infrastructure risk missing the phase where stablecoin volume consolidates into dominant rails.

What This Article Will Explore

• Why stablecoins are redefining digital settlement in banking

• How traditional banks are deploying tokenized deposits to defend transaction flows

• Why neobanks can move faster in integrating programmable settlement rails

• Where infrastructure debt slows incumbents, and where regulatory capital slows challengers

• Which model is structurally advantaged in the 2026 consolidation cycle

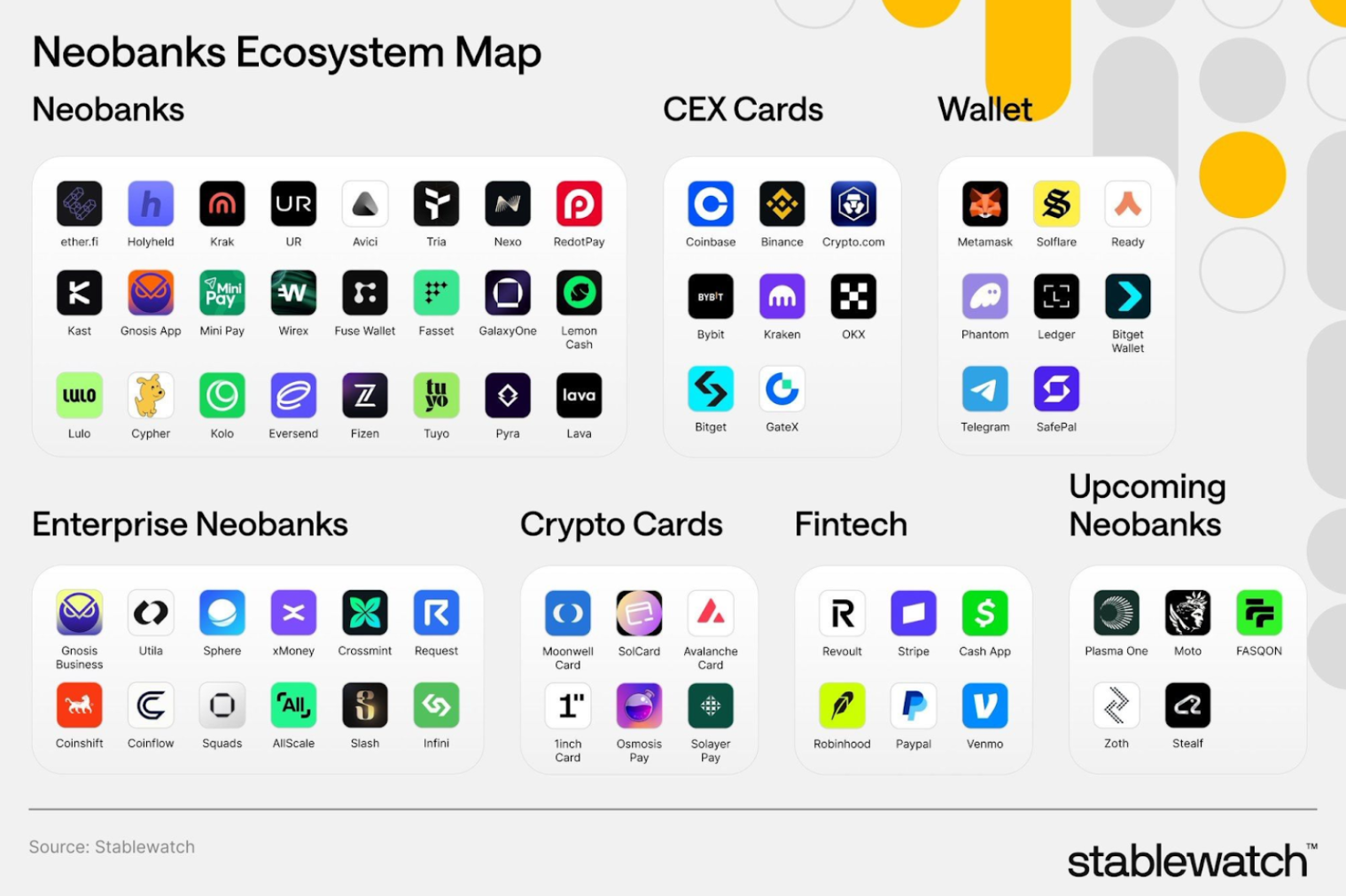

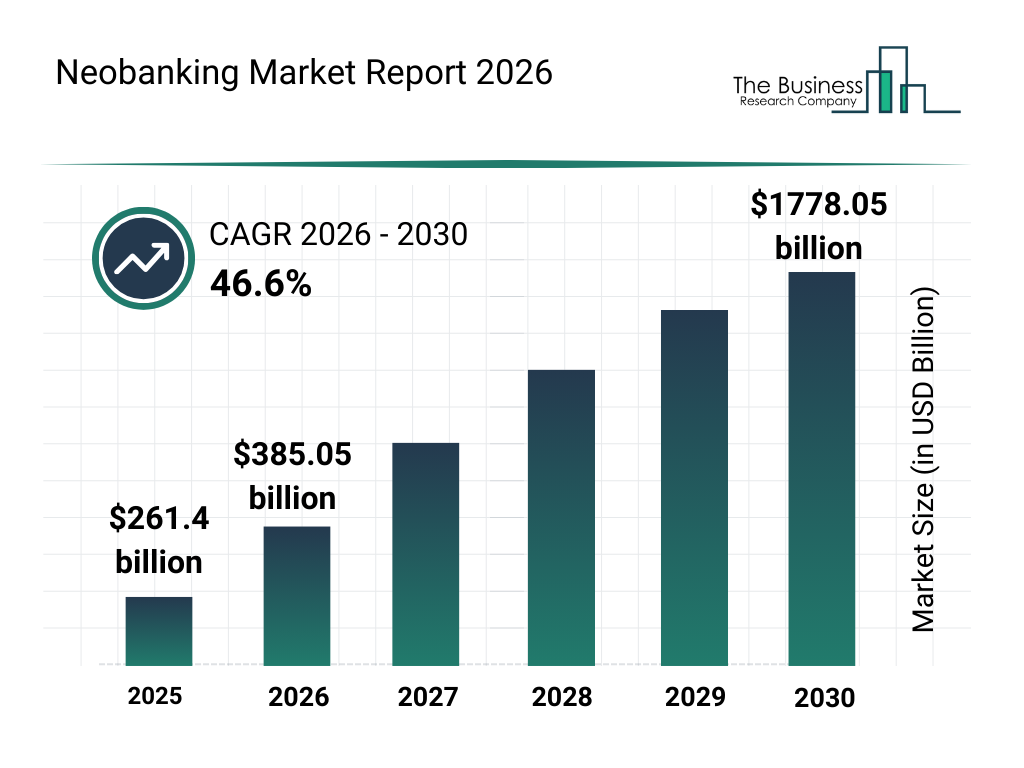

The Neobank Renaissance: Why $550B is Just the Starting Line

Recent industry reports confirm that neobanking remains in a high-growth phase. According to the Neobanking Global Market Report 2026 by The Business Research Company, the global neobanking market is projected to grow from approximately $382.8 billion in 2025 to $552.0 billion in 2026, signaling accelerating global adoption.

The structural shift in neobanking is demographic before it is technological.

Generational Defaults: Why Gen Z and Millennials are Reshaping the Core Banking Logic

Globally, Millennials and Gen Z account for roughly 78% of neobank users (industry data 2026). This is not a marginal segment. In the US and Europe, around 80% of millennials prefer digital-first banking experiences), and approximately 99% of Gen Z use a mobile banking app monthly, with 45–50% managing finances exclusively via smartphone. The behavioral implication is critical: for younger cohorts, neobanks are not experimental secondary accounts. They are primary financial interfaces.

That shift compounds over time. As Gen Z transitions into full-time workforce participation, income inflows scale, and so does transaction throughput. Multiple market forecasts (e.g., Mordor Intelligence) project total neobank transaction value potentially reaching $8–13 trillion by the 2030s. The growth thesis is not speculative adoption — it is lifecycle monetization of digitally native cohorts.

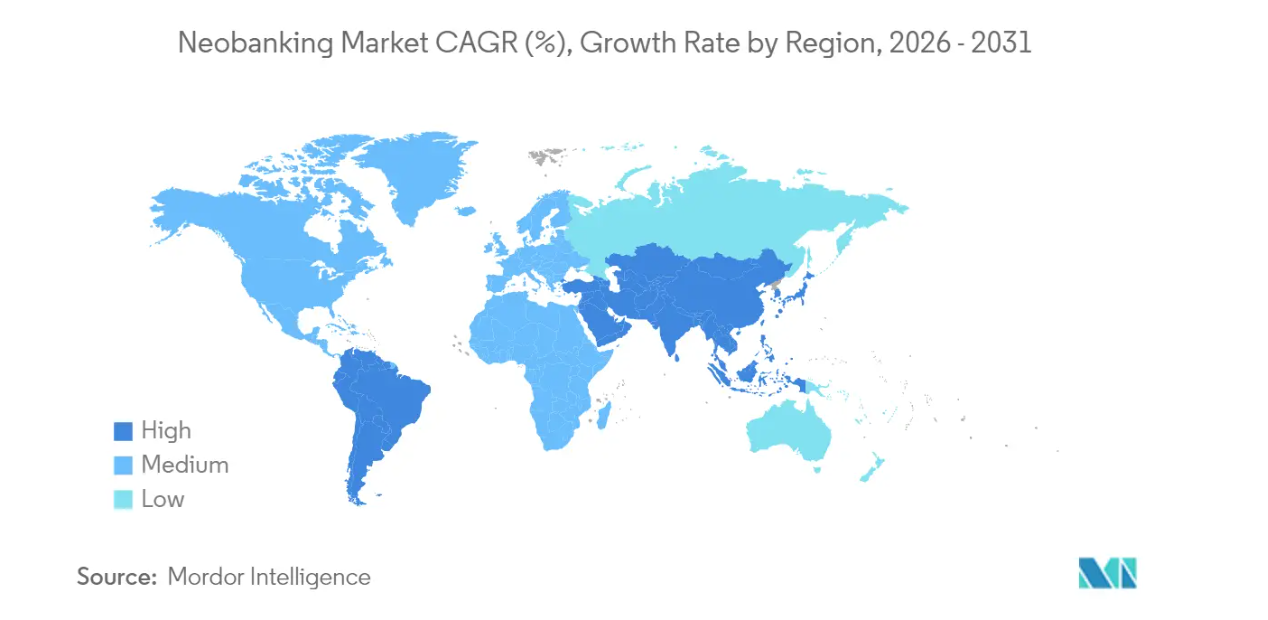

Regional Dynamics

Europe (~37% global market share)

Europe currently leads in market share, largely due to mature open banking frameworks (PSD2), interoperable payment rails, and regulatory encouragement of fintech competition. However, the same regulatory rigor increases compliance overhead. Rising capital requirements, safeguarding mandates, and AML complexity are already pushing consolidation. Smaller players struggle to maintain margin while scaling cross-border operations.

Asia-Pacific (Fastest CAGR, 51%+ in some reports)

APAC represents the highest growth velocity, driven by financial inclusion gaps and SME digitization across markets like India, Indonesia, and parts of Southeast Asia. Digital-native models scale rapidly where legacy banking penetration was weaker. The opportunity is structural: leapfrogging physical branch infrastructure into mobile-first ecosystems. However, regulatory fragmentation and heterogeneous KYC standards create operational complexity across jurisdictions.

United States

In the US, players like Chime and Revolut-style entrants have demonstrated revenue growth and improved profitability metrics in 2025–2026. Yet the competitive pressure is intensifying from incumbents modernizing their core systems. Large banks are experimenting with tokenized deposits and on-chain settlement infrastructure (e.g., JPMorgan’s deposit token initiatives), reducing the innovation gap that initially advantaged neobanks. The differentiation window is narrowing.

What This Means Structurally

The macro narrative is clear:

- Demographic adoption is durable.

- Transaction volume will scale materially over the next decade.

- Regional growth remains strong but increasingly regulated.

- Incumbents are no longer technologically stagnant.

Neobanks are entering a phase where scale is no longer enough. Growth in users and transaction value will expose deeper constraints in custody, compliance automation, capital efficiency, and cross-rail interoperability - especially as traditional banks move on-chain and settlement expectations compress from T+2 toward near real-time or atomic settlement models.

In short, demand-side momentum is secured. The real competitive bottleneck is shifting to infrastructure resilience and regulatory-grade execution.

Neobank Leaders Are Still Scaling Rapidly

If the sector were cooling, leading players would be slowing down.

The opposite is happening.

Chime

Chime raised its full-year 2025 revenue outlook in Q3 2025 after strong results:

- ~29% year-over-year revenue growth (Q3 revenue $544 million, full-year guidance raised to $2.163–$2.173 billion, implying 29-30% YoY).

- ~21% growth in active members (reached 9.1 million).

This demonstrates improving monetization efficiency (higher ARPAM, positive adjusted EBITDA) alongside user expansion, not just burn-driven growth.

Revolut

Revolut unveiled aggressive global expansion in Sep 2025:

- Targets 100 million retail customers by mid-2027 (from current ~65 million+).

- Committing £10 billion ($13 billion) in global investments over the next 5 years (including £3-4 billion in UK alone, creating 10,000 jobs worldwide).

This reflects an offensive, high-conviction strategy to enter 30+ new markets by 2030, far from defensive positioning.

Monzo

Monzo reported explosive profitability in FY2025 (year ended March 2025):

- Pre-tax profit surged ~335% to £60.5 million (from £13.9 million prior year; adjusted PBT up ~719% to £113.9 million in some metrics).

- Revenue topped £1.2 billion for the first time (up 48%), with strong growth in deposits (£16.6 billion) and lending.

This indicates unit economics improving at scale, profitability pivot, not mere capital-burn growth. (Note: The original ~300% often rounds the reported surge; some sources cite 300–335% depending on base.)

Three signals are converging:

- Market size continues expanding rapidly

- User adoption remains strong and generationally anchored

- Leading neobanks are scaling aggressively

In platform economics, this pattern often precedes:

- Market consolidation

- Higher customer acquisition costs

- Rising compliance barriers

- Infrastructure arms races

The strategic question is no longer whether the opportunity exists.

It is whether new entrants can build fast enough to compete before incumbents and scaled neobanks solidify their advantage.

In a market growing at 20-30% CAGR,

a 24-36 month infrastructure build delay is not neutral.

It is strategic exposure.

Traditional Banks on Blockchain: How Incumbents are Adopting Programmable Settlement Rails

If the first half of the 2010s was about neobanks challenging incumbents, the mid-2020s are about incumbents adapting aggressively, not by resisting change, but by integrating blockchain and tokenization into their core operations.

Traditional banks are no longer ignoring digital challengers. They are restructuring around them.

According to the BIS Annual Economic Report on Next‑Generation Monetary Systems, tokenization and digital settlement infrastructures are no longer experimental initiatives but core strategic priorities. The report argues that tokenised commercial bank money and central bank reserves can form the foundation of a more integrated, programmable financial system that reduces settlement friction and enables new financial instruments.

Meanwhile, central banks worldwide are actively testing digital currency infrastructure. Multinational projects such as mBridge - a multiple CBDC platform backed by the Hong Kong Monetary Authority, Bank of Thailand, UAE Central Bank, BIS Innovation Hub and others - are designed for real-time cross-border payments, explicitly showing sovereign infrastructure evolution.

Major global banks are also moving beyond experimentation.

For example, Alibaba to Use JPMorgan’s Blockchain for Tokenized Dollar and Euro Payments reports that JPMorgan is working with Alibaba to use tokenized deposits (digital versions of USD and EUR backed by the bank) over blockchain rails to speed settlement and reduce intermediaries in cross-border commerce - a practical example of incumbents adopting on-chain tools.

These efforts extend beyond wholesale trade. Mastercard and JPMorgan Link Up to Bring Cross‑Border Payments on the Blockchain describes how Mastercard’s Multi-Token Network is integrating with JPMorgan’s Kinexys Digital Payments platform to deliver faster, API-ready settlement systems, indicating that traditional payment giants are also joining the shift.

The implication is clear:

Neobanks are no longer competing only against “slow, branch-based banks.”

They are competing against incumbent banks with digital, programmable rails.

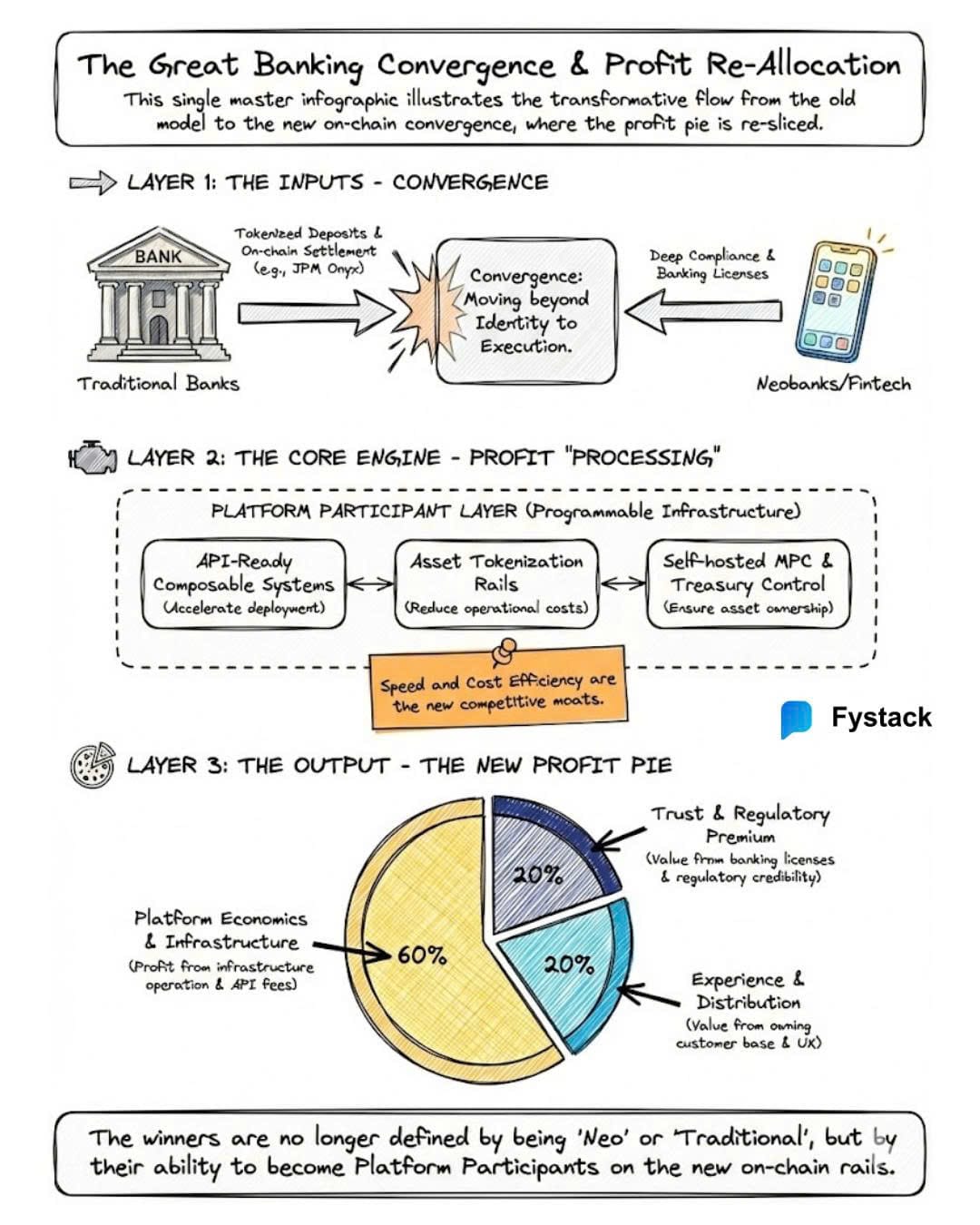

The Banking Profit Pool Re-Allocation: From Product Sellers to Platform Participants

The global banking profit pool - spanning deposits, FX margins, cross-border fees, card interchange and lending - remains large, but the share captured by different players is shifting.

Historically, traditional banks relied on fee spreads and legacy services as primary revenue. Today, digital challengers compress fees while platform-style infrastructure providers capture backend economics. Analysts like fintech strategist Chris Skinner argue that banks are evolving from “product sellers” to “platform participants,” where API capability, composability and digital integrations determine competitive positioning.

Similarly, research from institutions such as the Basel Committee on Banking Supervision (BIS) Report on digital entrants and bank business models notes that innovative technologies allow new digital entrants to offer services at lower operational cost and higher speed than legacy platforms, forcing incumbents to upgrade infrastructure.

What this means in practice:

The “pizza” of banking profits is not disappearing - it is being re-sliced.

Neobanks captured early growth by improving UX and reducing fees.

Now, incumbents are reclaiming ground by modernizing core rails and integrating digital asset technologies.

Convergence, Not Replacement

The narrative that “neobanks will replace traditional banks” is too simplistic.

Instead, the market is experiencing convergence:

- Traditional banks are launching digital subsidiaries and tokenized products. JPMorgan’s on-chain offers include tokenized deposit tokens and settlement pilots expanding toward broader blockchain deployment.

- Neobank players are deepening compliance integration to operate with full banking licenses and regulatory frameworks.

- Both sides are investing in programmable infrastructure - whether through private ledgers adapted to public rails, or API-ready composable systems.

This convergence intensifies competition.

The next winners will not be defined by whether they are “neo” or “traditional,”

but by:

- Speed of infrastructure deployment

- Cost efficiency of core systems

- Ability to integrate new settlement rails and APIs

- Capacity to launch financial products rapidly

The market is no longer divided by identity.

It is divided by execution speed.

6 Transformational Trends Shaping the Future of Crypto Neobanking in 2026

Crypto neo banking in 2026 is no longer defined by wallets, cards, or token support. The transformation happening now is architectural. What is changing is not just the interface users see, but the financial logic that operates underneath. These shifts matter because they redefine how platforms must be built, how capital flows, and how competitive advantage is created.

Below are six structural trends shaping the next phase of crypto-native banking.

Finance is moving from user-driven execution to system-driven optimization.

Artificial intelligence in banking has historically been limited to automation and chat interfaces. In 2026, the shift is toward agentic systems - AI models capable of making real-time financial decisions on behalf of users within predefined parameters.

Instead of asking users to manually choose networks, manage gas fees, or compare exchange rates, intelligent systems now evaluate:

- Network congestion

- Transaction costs

- FX spreads

- Settlement speed

- Liquidity availability

For example, when a business pays an overseas contractor, the system can automatically determine whether to route funds through a stablecoin corridor, convert through a centralized exchange, or use a faster L2 settlement path-optimizing for cost and speed without manual intervention.

This is not speculative. Financial institutions globally are investing heavily in AI integration for transaction monitoring, liquidity forecasting, and fraud detection. AI-enabled financial services are increasingly positioned as operational infrastructure rather than experimental tools.

The implication is architectural: if your core infrastructure cannot support programmable execution layers, you cannot implement agentic finance effectively.

Collapsing the Crypto-Fiat Divide with Unified Asset Dashboards

For years, financial apps separated “crypto” from “banking.” That separation is becoming artificial.

Modern users hold:

- Stablecoins

- Fiat balances

- Tokenized assets

- Traditional investment instruments

What they want is unified visibility and control.

Hybrid financial accounts now present all assets within a single dashboard. More advanced platforms enable automatic allocation rules-allowing users to define portfolio preferences that rebalance dynamically.

This model resembles automated wealth management, but democratized for broader audiences. Instead of manually converting between fiat and crypto, the system handles allocation logic in the background.

The architectural implication is significant: ledger systems must support asset abstraction layers capable of handling both traditional and tokenized value representations without fragmenting the user experience.

Stablecoins are becoming transactional primitives rather than trading instruments.

Stablecoins were initially associated with crypto trading and volatility hedging. Increasingly, they function as:

- Settlement rails

- Treasury instruments

- Yield-bearing cash equivalents

Major financial institutions and payment networks have explored stablecoin pilots and tokenized deposits in recent years, signaling broader acceptance of digital settlement mechanisms.

For users, this manifests in practical ways:

- Idle balances earning yield through tokenized treasury exposure

- Cross-border remittance corridors built on stablecoin rails

- Payroll and B2B settlement using programmable tokens

This trend matters because it changes the economics of holding money. Checking accounts that generate yield through stablecoin infrastructure alter consumer expectations about passive capital efficiency.

For builders, supporting stablecoins is no longer optional. It requires treasury logic, liquidity management, and regulatory alignment embedded into the infrastructure layer.

The winners in crypto neo banking will be defined by how effectively they abstract complexity.

Each of the trends above-AI agents, embedded finance, cross-border optimization, hybrid asset management, and stablecoin infrastructure-requires deep backend coordination.

Individually, these systems are complex. Together, they form a multi-layer financial operating system:

- Deterministic ledger engines

- Multi-rail settlement orchestration

- Compliance and risk synchronization

- Asset abstraction layers

- AI execution hooks

Building this entirely in-house is technically possible. But in a market expanding rapidly and consolidating around scaled players, the opportunity cost of long internal build cycles becomes strategic.

The emerging divide in 2026 is not between “crypto” and “traditional” banks. It is between:

- Teams that must engineer financial plumbing before launching

- Teams that can integrate programmable infrastructure and deploy capital toward growth

Infrastructure abstraction-turning regulated financial complexity into composable APIs-is not a shortcut. It is becoming the foundation for execution speed.

The choice between building on a vendor's runtime or owning the execution environment is a defining strategic decision. A deep dive into these architectural trade-offs is available in Fystack vs Fireblocks – Self-Hosted vs SaaS, which analyzes why self-hosted models are becoming the gold standard for institutions seeking true data sovereignty.

And in a consolidating market, execution speed compounds.

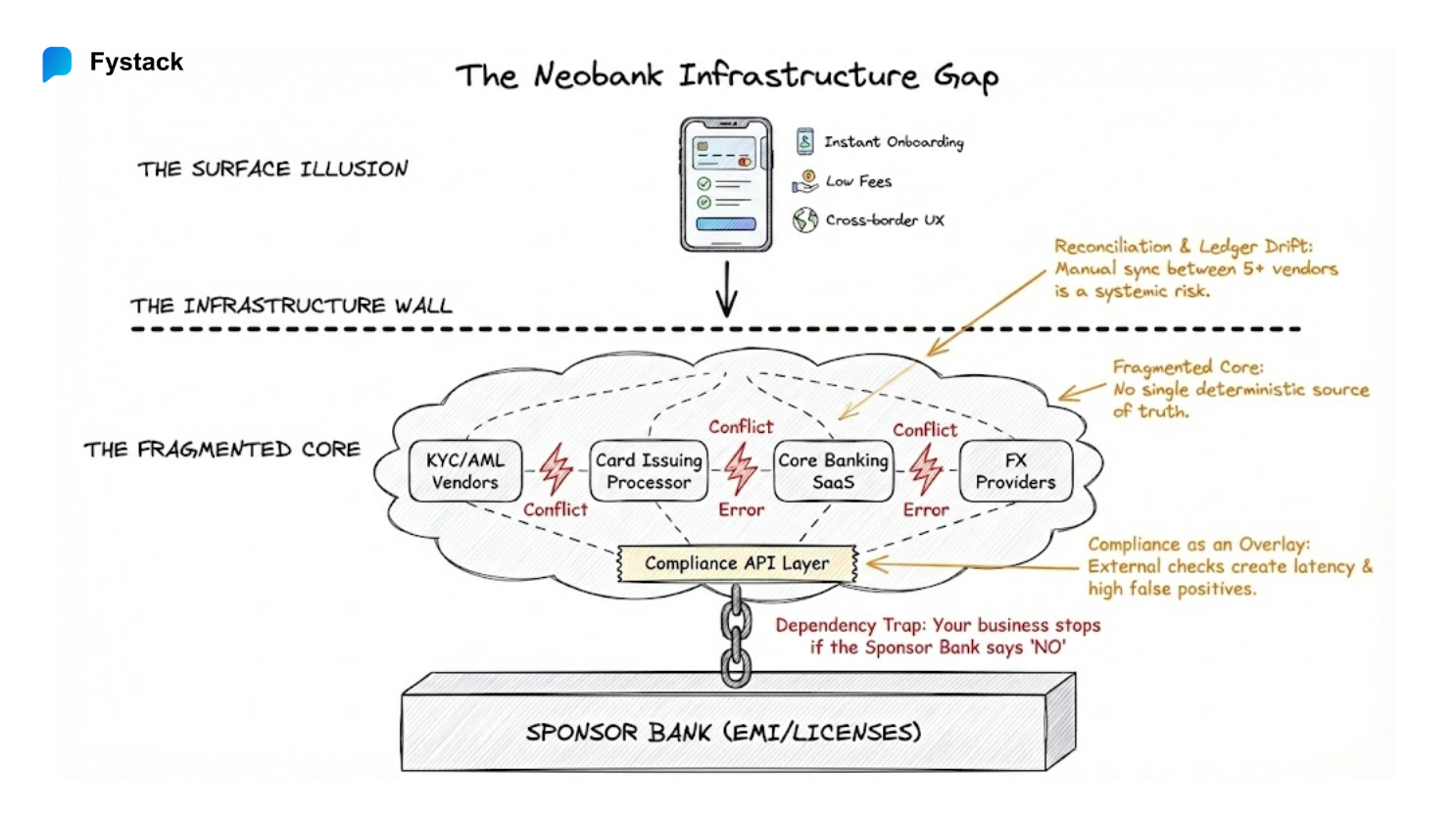

Beyond the UX: The Infrastructure Challenges Limiting Modern Neobanks

Over the past decade, neobanks have positioned themselves as faster, more user-centric alternatives to traditional banks. Sleek UX, instant onboarding, low fees, and cross-border capabilities helped them win early adoption. But beneath that front-end agility sits a structural reality: most neobanks do not own their core infrastructure.

As the market matures and traditional banks modernize their own stacks - including moving parts of their operations on-chain or into real-time settlement systems - the infrastructure weaknesses of neobanks are becoming increasingly visible.

The core problem is not growth. It is architecture.

1. Fragmented Core Architecture

Most neobanks are built as orchestration layers rather than true financial systems.

A typical stack includes:

- A sponsor bank providing regulatory cover and holding deposits

- A card issuing processor

- A core banking SaaS

- KYC and AML vendors

- Fraud monitoring APIs

- Cloud-hosted application logic

Each component works independently, often provided by different vendors, each with its own SLA, data model, and failure surface.

In the early stage, this modularity accelerates launch. But as transaction volumes scale, this fragmentation becomes operationally fragile. Ledger reconciliation becomes complex because data must be synchronized across systems that were never designed as a single deterministic source of truth. Incident resolution becomes slower because root causes span multiple vendors.

The result is structural: the neobank does not fully control its own financial engine.

Traditional banks, in contrast, historically built around a tightly controlled core ledger. Even if legacy systems were slow, they were internally unified. Neobanks often lack that unification.

2. Sponsor Bank Dependence and Structural Vulnerability

A significant number of neobanks operate without full banking licenses. Instead, they rely on sponsor banks or EMI partnerships to access payment rails and regulatory coverage.

This dependency introduces a systemic vulnerability. If the sponsor bank adjusts its risk appetite, changes compliance interpretation, or tightens capital requirements, the neobank must adapt immediately often without negotiation leverage.

There have been multiple cases globally where fintech programs were paused or terminated because sponsor banks reassessed risk exposure. When this happens, the neobank’s users experience service disruption even though the neobank itself did not fail technically.

This reveals a deeper infrastructure weakness: the neobank does not control the ultimate settlement layer or deposit custody. It controls the interface, but not the core.

As traditional banks begin integrating real-time settlement and even tokenized deposit systems, their control over both capital and infrastructure widens the competitive gap.

3. Reconciliation and Ledger Inconsistency at Scale

As transaction volumes grow, reconciliation complexity becomes one of the most underestimated infrastructure burdens.

Neobanks must reconcile across:

- Internal ledger systems

- Card network settlement cycles

- Payment processors

- FX providers

- Potentially blockchain networks if stablecoins are integrated

Each of these systems operates on different timing conventions and reporting structures. Cut-off times differ. Settlement latency differs. Error handling differs.

At small scale, reconciliation discrepancies can be resolved manually. At scale, they become systemic risks. Ledger drift - even minor inconsistencies - creates regulatory exposure and erodes financial transparency.

Traditional banks invest heavily in deterministic accounting systems precisely to avoid this. Many neobanks, built on API-first orchestration layers, do not embed deterministic reconciliation into their architecture from day one.

Infrastructure debt accumulates quietly until growth amplifies it.

4. Compliance as an Overlay Instead of a Core Primitive

Regulatory scrutiny has intensified across jurisdictions. AML, sanctions screening, transaction monitoring, data residency, and reporting obligations have expanded significantly.

Many neobanks integrate compliance through third-party APIs layered on top of transaction systems. This means compliance checks are externalized rather than embedded directly into the transaction execution logic.

When regulatory pressure increases- for example, stricter real-time monitoring requirements or enhanced travel rule enforcement - the compliance layer becomes a bottleneck. False positives increase operational workload. Investigation teams grow. Latency increases.

Traditional banks have compliance deeply integrated into their core systems because they evolved under regulatory pressure. Neobanks, designed for speed, often retrofit compliance after scaling.

As banks move toward on-chain or real-time programmable settlement systems, compliance logic is increasingly embedded at the infrastructure layer. Neobanks that do not evolve their architecture face rising operational and regulatory costs.

Navigating the 2026 regulatory landscape requires a shift from reactive monitoring to embedded enforcement. Our 2026 Crypto Compliance: Global Stablecoin Laws & Fintech Checklist provides a comprehensive framework for aligning programmable payments with evolving international standards.

Infrastructure Sovereignty: Why Neobanks are Switching to Self-Hosted MPC Solutions

The competitive landscape is shifting. Traditional banks are modernizing. Real-time payment rails are expanding. Tokenized deposits and on-chain settlement experiments are increasing among incumbents.

This changes the battlefield.

If both banks and neobanks operate with comparable digital rails, then differentiation shifts from UX to infrastructure ownership:

- Who controls settlement deterministically?

- Who embeds compliance directly into execution logic?

- Who owns custody and capital access?

- Who can optimize cost structure at scale?

Neobanks that remain orchestration layers risk being compressed into thin-margin application providers.

Neobanks that move toward deeper infrastructure control - whether through building or partnering with infrastructure-grade providers - gain:

- Greater sovereignty over operations

- Reduced vendor fragmentation

- Embedded compliance capabilities

- Improved margin resilience

In other words, infrastructure is no longer a backend concern. It is a competitive strategy.

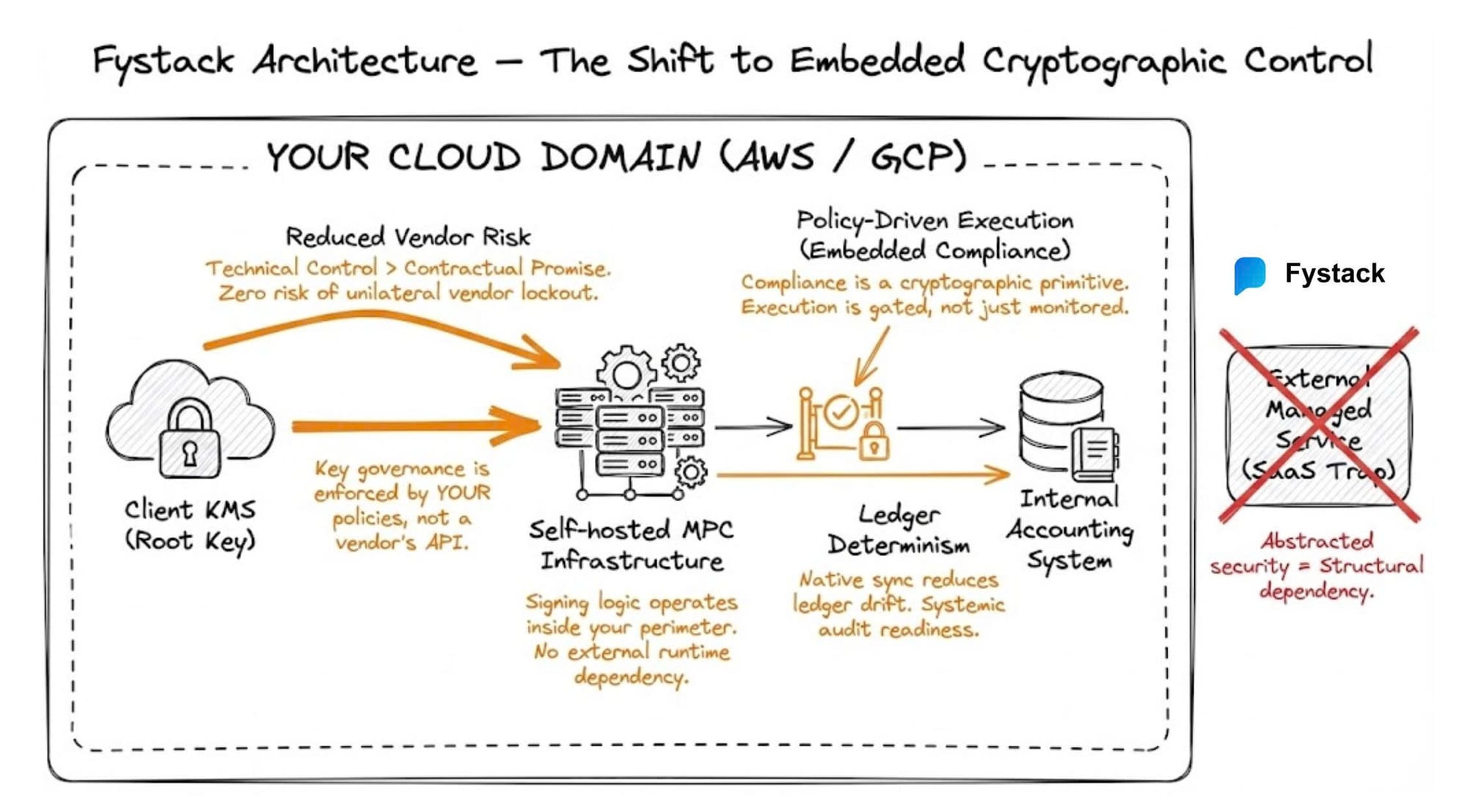

Fystack Architecture: Embedding Cryptographic Control Within Your Own Domain

If the structural weakness of many neobanks is fragmentation across custody, compliance logic, and settlement orchestration, then the problem is not which additional vendor to integrate next. The deeper issue is whether the architecture itself needs restructuring.

Fystack positions itself at that architectural layer.

Rather than operating as another SaaS interface on top of outsourced primitives, Fystack is built as a self-hosted MPC wallet infrastructure layer. It enables financial institutions and fintechs to retain deterministic control over cryptographic execution and digital asset custody inside their own cloud environment.

That architectural decision changes the control model.

Most custody providers operate as managed services. Even when MPC is used, the signing runtime often remains under vendor control. This simplifies integration but preserves structural dependency at the most sensitive boundary: transaction authorization.

Fystack runs inside the client’s own infrastructure, such as AWS or GCP, with key governance enforced by the client’s KMS policies. The cryptographic boundary is not abstracted behind an external runtime. It is embedded directly within the institution’s infrastructure domain.

In practical terms, this addresses several structural pressures facing neobanks:

• Reduced vendor concentration risk

Key generation, signing logic, and policy enforcement operate inside the institution’s environment. Exposure to third-party runtime outages or unilateral access restrictions is structurally minimized. Control becomes technical, not contractual.

• Policy-driven transaction execution

Compliance logic can be embedded directly into the signing workflow. Instead of layering AML checks after a transaction is initiated, execution can be gated cryptographically. This transforms compliance from reactive monitoring into embedded enforcement.

• Stronger ledger determinism and auditability

When signing authority integrates with internal accounting systems rather than relying on webhook confirmations from external custodians, reconciliation becomes systemic. This reduces ledger drift and improves audit readiness.

• Infrastructure consolidation instead of stack sprawl

Fystack operates as a foundational control layer that other systems integrate into. The objective is to centralize cryptographic governance, not add another external dependency.

Ready to automate your compliance and take control?

Sign up for Fystack now for exclusive access.

Join our Telegram Community to discuss compliance challenges and solutions with our team and other builders.

FAQ

Is the neobank market still growing, or approaching saturation?

The market remains in a high-growth phase. According to the Neobanking Global Market Report 2026 by The Business Research Company, the sector is projected to grow from approximately $382.8 billion in 2025 to $552.0 billion in 2026. Adoption is generationally anchored, particularly among Millennials and Gen Z, making demand structurally durable rather than cyclical.

Why is execution speed now more critical than market opportunity?

Demand is no longer the primary constraint. With 20–30% CAGR growth and transaction values projected into multi-trillion-dollar ranges, a 24–36 month infrastructure build delay creates strategic exposure. In a compounding market, slow deployment results in lost share that is difficult to recover once consolidation begins.

How are traditional banks responding to neobank competition?

Incumbents are modernizing core systems and integrating tokenized deposits and programmable settlement rails. Institutions like JPMorgan are deploying blockchain-based settlement infrastructure, while multinational initiatives such as mBridge demonstrate sovereign-level experimentation with real-time cross-border digital currency systems.

Are neobanks competing against legacy banks or digital banks?

Increasingly, they are competing against digitally modernized incumbents. The market is converging: traditional banks are adopting programmable rails, while neobanks are pursuing full regulatory licensing and embedded compliance. Competitive differentiation now centers on infrastructure control and deployment velocity rather than brand identity.

What are the biggest infrastructure weaknesses limiting neobanks?

Many neobanks operate as orchestration layers across sponsor banks, payment processors, compliance vendors, and SaaS core systems. This fragmentation introduces reconciliation complexity, vendor concentration risk, compliance latency, and limited control over deterministic settlement.

Why is sponsor bank dependence considered a structural risk?

Neobanks without full licenses rely on sponsor institutions for regulatory coverage and deposit custody. Changes in sponsor risk policy or compliance interpretation can directly impact operations, even if the neobank itself remains technically sound. This exposes a dependency at the settlement and capital layer.

What does “infrastructure sovereignty” mean in crypto neobanking?

Infrastructure sovereignty refers to owning deterministic control over custody, transaction authorization, compliance logic, and settlement orchestration within the institution’s own environment. It shifts control from vendor-managed runtimes to internally governed cryptographic execution systems.

How do self-hosted MPC models differ from SaaS custody solutions?

In SaaS custody models, signing infrastructure often remains under vendor-managed runtime control. Self-hosted MPC architectures embed key governance and signing workflows directly within the institution’s cloud environment, reducing third-party runtime dependency and improving auditability and compliance integration.

Why are stablecoins becoming infrastructure rather than speculative tools?

Stablecoins increasingly function as settlement rails, treasury instruments, and programmable payment primitives. As institutions experiment with tokenized deposits and yield-bearing digital assets, stablecoins shift from trading instruments to core components of transactional finance.

What will define the next winners in the neobank market?

The decisive factors are infrastructure deployment speed, embedded compliance automation, cost-efficient core systems, and the ability to integrate programmable settlement rails. In a consolidating market, execution velocity compounds faster than branding advantages.