APAC Fintech and the Compliance Squeeze: The Hidden Cost of Add-On KYT

TL;DR APAC fintechs currently face a growing compliance gap: regulations are tightening across Southeast Asia, while many firms still rely on third-party KYT integrations. This creates compliance debt, data sovereignty risks, and operational inefficiencies. The long-term solution is custody infrastructure with KYT built into the core signing layer from day one.

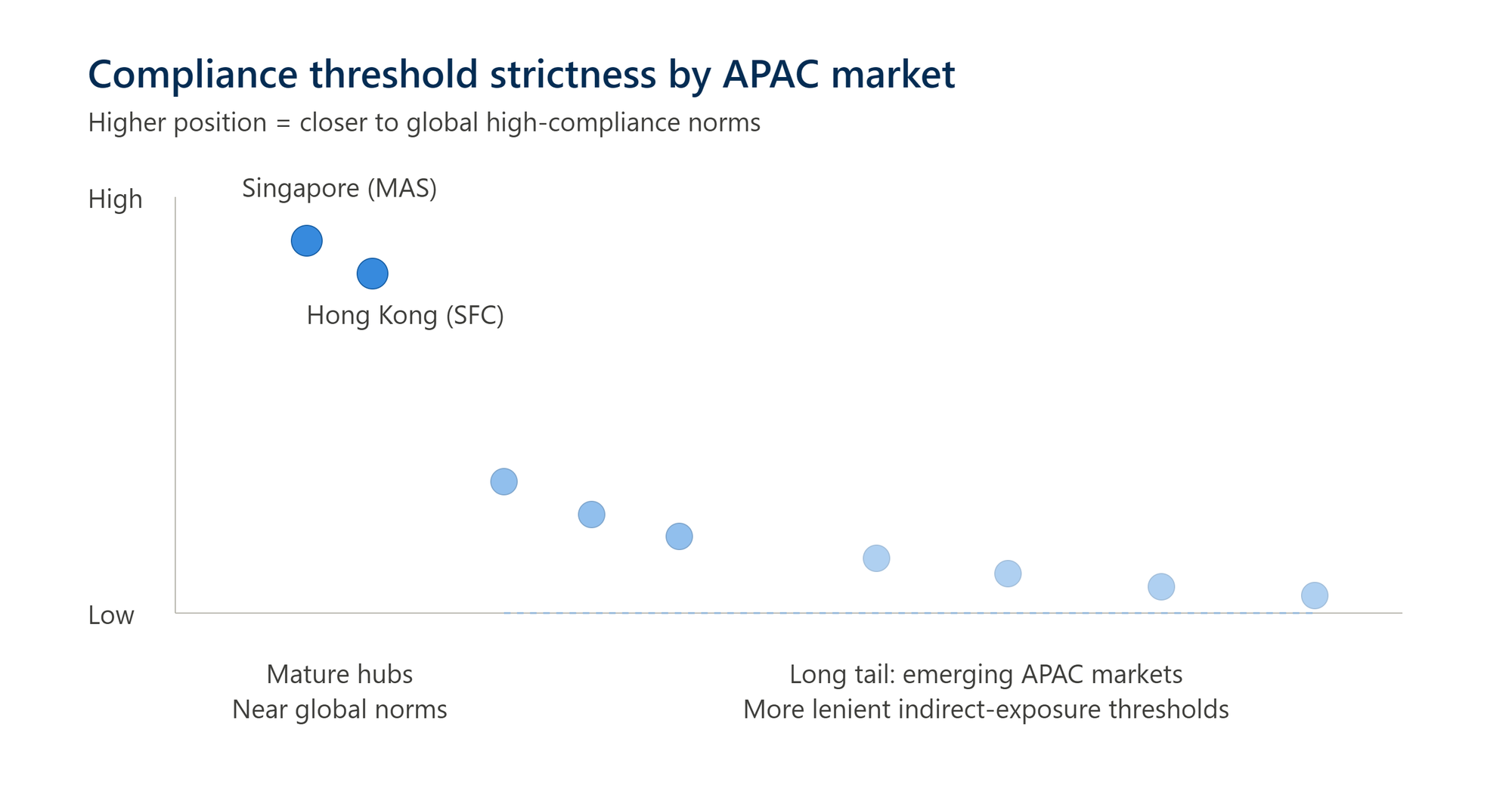

A recent benchmark report from Chainalysis, built on Know-Your-Transaction (KYT) data from hundreds of organizations worldwide, surfaced a finding worth sitting with: the crypto industry's compliance baseline has tightened sharply over the past few years, but the pace of that tightening is far from even across regions. APAC sits at the loose end of the spectrum.

For a fast-growing fintech, "looser" might sound like an advantage: less friction, faster time to market, lower compliance overhead. But that is a short-term read. The gap is not a lasting privilege. It is debt quietly accumulating, and it tends to come due exactly when a company is least prepared for it: right after it has scaled.

1. The "easy" advantage is disappearing

According to Chainalysis data, mature markets like the Americas (AMER) and Europe/Middle East/Africa (EMEA) show tightly clustered, high alerting thresholds, meaning most organizations there are effectively forced to operate near strict compliance norms. APAC tells a different story: a right-skewed distribution, where only a small cluster of jurisdictions with established frameworks (Singapore under MAS, Hong Kong under SFC) sit near that high bar, while a long tail of other markets across Southeast and South Asia still operates with materially more lenient monitoring.

That gap is the "low ground" many APAC fintechs have leaned on to grow fast: cheaper compliance, quicker onboarding, fewer upfront barriers. It is also the most exposed position to be in once the regulatory tide turns.

And that tide is no longer a distant forecast. It is already moving, faster than most product teams realize.

Vietnam is the clearest case. For nearly a decade, crypto in Vietnam sat in legal limbo: not explicitly banned, but without a formal framework, leaving banks and exchanges to operate in a gray zone. That changed on January 1, 2026, when the Law on Digital Technology Industry took effect, formally recognizing digital assets as property under the Civil Code for the first time. Fystack covered this shift as it was unfolding in a post on the new legal corridor for crypto businesses in Vietnam. Alongside it, Resolution 05/2025/NQ-CP established a five-year pilot program (2025 to 2030) for crypto asset issuance and trading, setting a minimum charter capital requirement of VND 10 trillion (roughly $380 to $400 million) for licensed Crypto Asset Service Providers (CASPs), a bar higher than commercial banking capital requirements in many countries. Notably, the resolution also prohibits the issuance of fiat-backed stablecoins domestically, meaning USDT- or USDC-style models are not yet recognized under the new framework, and all trading must run through licensed domestic CASPs.

Thailand has taken a different but parallel route: tightening in stages rather than all at once. The Securities and Exchange Commission (SEC) has required exchanges, brokers, and custodians to be licensed and meet capital and AML/KYC standards since 2018. More recently, under Thailand's Cybercrime Law, digital asset operators are required to share information, screen and suspend transactions or accounts tied to cybercrime, and blacklist associated wallet addresses. A dedicated stablecoin framework is also in development, though not yet finalized.

Indonesia is following the same direction of tightening oversight. On January 10, 2025, supervisory authority over crypto moved from the commodities regulator (Bappebti) to the Financial Services Authority (OJK), formally bringing crypto into the financial supervision perimeter with stricter capital and consumer-protection rules. One detail stands out: under OJK's framework, crypto asset traders onboarding non-individual (institutional) clients must already have systems in place that implement Know-Your-Transaction (KYT) principles. KYT is no longer a "nice to have." It is becoming a licensing condition in one of the region's largest markets.

Three markets, three different paths, one shared direction: legal frameworks are being codified faster, compliance requirements are getting more specific, and the "regulatory gap" many fintechs once relied on to grow quickly is shrinking quarter by quarter.

The practical consequence: a fintech that optimizes short-term by skipping rigorous transaction monitoring is not actually saving money. It is deferring the cost, with interest. Retrofitting compliance onto a system already running at scale is always more expensive and riskier than building it into the infrastructure from day one.

To make the regional gap concrete, here is how the compliance distribution looks across APAC versus a handful of mature hubs:

2. The fatal mistake: "we'll bolt it on when we need it"

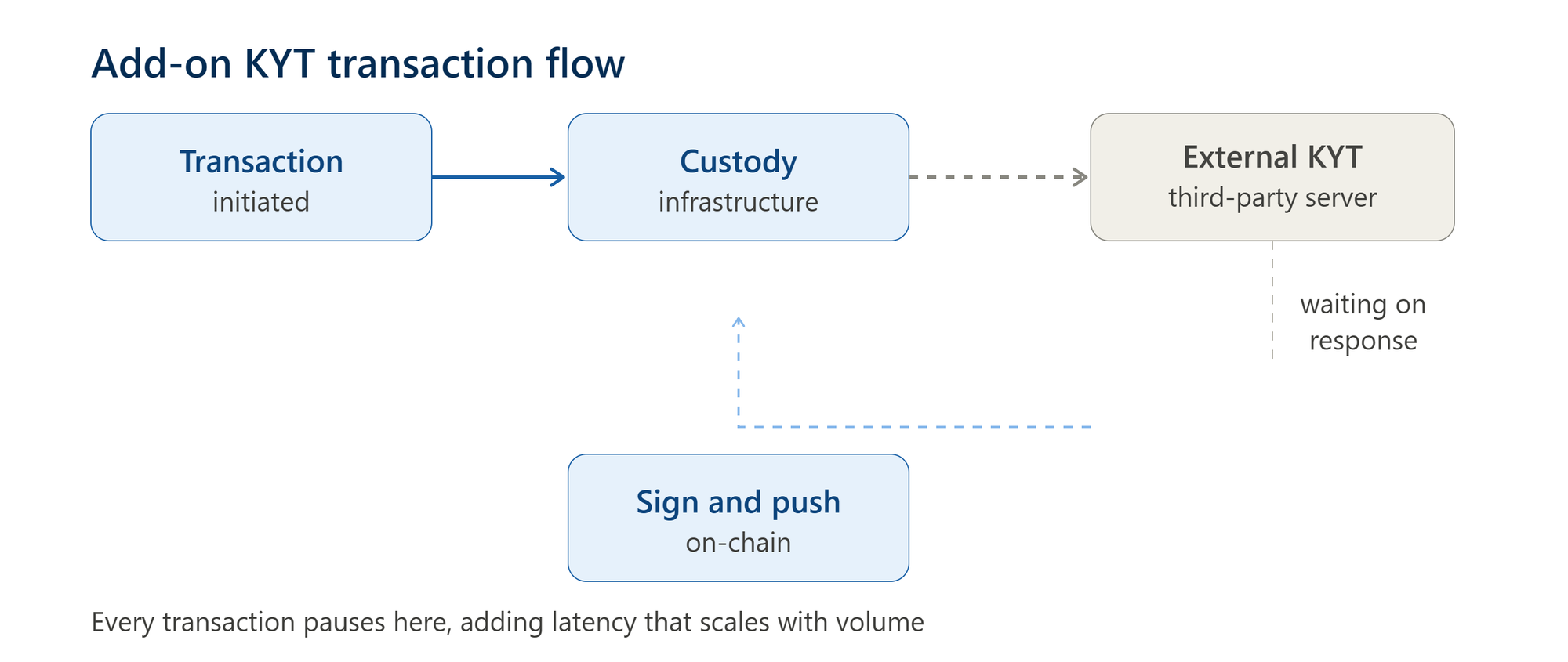

The most common way fintechs currently handle compliance is to keep their existing custody or wallet stack and attach a third-party KYT layer through an API once a regulator or banking partner requires it. Operationally, this is the fastest way to "check the box." But it creates three problems that few teams see coming until they are already too deep to turn back.

System friction. Custody and KYT are built by two different vendors, following two different design logics. Stitching them together over an API always carries integration risk, and when that risk surfaces at the transaction-processing layer, the consequence is not just a bug. It is a real compliance or operational exposure. Either vendor can change an API schema or risk-scoring logic without warning, breaking the integration in ways neither team notices right away, because neither side owns the full end-to-end flow. The fintech's own engineering team, which built neither system, becomes the tape holding the middle together, patching a piece of architecture they do not fully control.

Latency that wrecks the user experience. When the KYT layer runs as an independent service, separated from the signing process, every transaction has to pause and wait for a risk-scan response from an external system before it can proceed. At meaningful volume, this is a real bottleneck: it can increase processing time, raise failure or slippage rates, and degrade the end-user experience. For stablecoin payment or remittance products, where speed is part of the value proposition, a slow or briefly unavailable third-party KYT service means the entire payment flow stalls, not because of a custody failure, but because of an external dependency that did not respond in time.

Layered hidden costs. Separate licensing for custody, separate per-transaction fees for third-party KYT scanning, plus the engineering cost of maintaining an integration layer between two systems that were never designed to work together. And when something breaks, operations teams end up doing more manual work to compensate for what the system cannot automate. This is the cost category fewest companies budget for upfront, and it is the one that grows fastest as transaction volume scales. A related cost that is often missed during planning: manual alert handling. When KYT sits outside the custody stack, every risk flag needs a human to review and decide before a transaction can proceed or be rejected, a process that does not automate cleanly unless the two systems communicate directly at the moment of signing.

Together, these three issues are not just engineering overhead. They are operational risk compounding over time, and the longer a system runs in production at scale, the harder it becomes to unwind. Fystack's own breakdown of how crypto off-ramps work walks through this same problem from the payout side: compliance sits as one of five layers between an on-chain deposit and a successful bank payout, and if that layer is bolted on rather than built in, it is usually the layer that breaks first when volume spikes.

Real-world enforcement: the cost of complacency

If the idea of regulators still being in an "educational phase" feels reassuring, the enforcement record from late 2025 into 2026 tells a different story.

In October 2025, Canada's financial intelligence agency, FINTRAC, issued its largest-ever penalty: roughly CAD 177 million (about USD 126 million) against Xeltox Enterprises Ltd., operator of the crypto payments platform Cryptomus. According to FINTRAC's findings reported by CBC News, the firm failed to flag more than 1,000 transactions with suspected ties to criminal activity, including funds connected to darknet markets, ransomware, and sanctions evasion, and did not report thousands of transactions originating from Iran despite a ministerial directive requiring enhanced scrutiny. Reporting from BetaKit noted the company had "incomplete and inadequate policies and procedures" governing ongoing monitoring and know-your-client obligations. This was not a US sanctions case; it was a Canadian AML regulator acting on a payments platform whose monitoring controls simply did not keep pace with the volume and risk profile of what was passing through it. For any fintech leaning on a thin, bolted-on compliance layer, the lesson is the same regardless of which country's regulator eventually looks: gaps in monitoring do not stay invisible forever, and the penalty scales with how long they went unaddressed.

A separate but related finding came from inside the industry itself. In July 2025, MetaComp, a Major Payment Institution licensed by the Monetary Authority of Singapore, published a study analyzing 7,000 live USDT and USDC transactions across Ethereum and Tron, screened through four leading KYT providers (Chainalysis, Elliptic, Merkle Science, and Beosin). The finding, reported by MetaComp itself and covered independently by ITBrief Asia: relying on only one or two KYT data providers let up to 25% of high-risk transactions slip through undetected. Worth being precise here: this study is about data-source coverage, how many independent KYT vendors screen a transaction, not about where in the architecture screening happens. It does not directly test add-on versus built-in models. What it does show is that compliance coverage is fragile by default, even for a fully licensed institution. That fragility compounds when the screening layer is also disconnected from signing, since a missed detection in an add-on model has no second checkpoint before the asset leaves the wallet. A built-in model does not solve MetaComp's data-coverage problem, but it closes the structural gap next to it: even a well-run KYT engine cannot help if there is no guaranteed checkpoint between detection and signing.

Enforcement signals, late 2025 to early 2026

-------------------------------------------------------

FINTRAC vs Cryptomus (Oct 2025)

Record CAD ~177M penalty for failing to flag

transactions tied to darknet markets, ransomware,

and sanctions evasion

MetaComp KYT coverage study (Jul 2025)

Up to 25% of high-risk transactions missed when

screened by only one or two KYT data sources

Regional policymaking is following the same trajectory. Asian central bankers and regulators have signaled a more coordinated, less permissive posture toward digital asset oversight, a shift reported across regional financial media in 2026, echoed in PwC's global crypto regulation tracking, which describes the market moving past the design phase of digital asset rules into active supervision. Travel Rule compliance specifically is becoming its own cost center: research on APAC Travel Rule compliance solutions points to growing demand for tooling that can produce a defensible, auditable record of when a screening decision happened relative to when a transaction was signed, exactly the kind of evidentiary gap an external, asynchronous KYT add-on struggles to close cleanly. Chainalysis's own explainer on the Travel Rule covers why originator and beneficiary information needs to travel with a transaction, a requirement that gets harder to satisfy when screening and signing live in two separate systems with two separate logs.

The throughline across all three signals: regulators are no longer satisfied with a checkbox. They are starting to look at the architectural depth of how monitoring actually works, down to the sequencing between a risk check and a signature.

Why this is a business problem, not just a compliance one

It's tempting to file all of this under "legal risk" and move on. But weak transaction monitoring quietly erodes the business itself in three concrete ways.

It closes the door to enterprise revenue. Many APAC fintechs grow their first wave of volume through retail users or small merchants, where compliance scrutiny is comparatively light. Reaching profitability at scale, though, usually means winning enterprise and B2B contracts: payment rails for large e-commerce platforms, logistics companies, or institutional treasuries. These counterparties run real due diligence before signing, and a custody stack that depends on a patched-together add-on, with occasional latency-driven slippage and no clear answer on where customer data physically lives, gets quietly removed from the shortlist before the conversation even starts.

It threatens the banking relationship the whole business depends on. Every stablecoin or crypto payment fintech relies on a banking partner willing to clear fiat on-ramp and off-ramp traffic. Banks are under their own "de-risking" pressure from regulators above them. If a bank's own monitoring flags that funds moving through a fintech's rails touched a sanctioned or high-risk wallet, because a single add-on KYT layer missed it, the response is rarely a warning. It is account closure, a frozen payment gateway, or a sudden multiple-times increase in processing costs. For a payments business, losing the banking relationship is close to a business-ending event.

It erodes margin precisely when the business is succeeding. In an add-on SaaS model, third-party KYT fees are typically charged per transaction, so the compliance cost line scales close to linearly with volume, compressing margin exactly when the business is growing fastest. In a self-hosted, built-in model, the infrastructure cost is closer to fixed: the heavier engineering investment happens once, and additional volume runs through the same infrastructure without a proportional new fee per transaction. The growth curve that erodes margin under one model is the same curve that improves margin under the other.

3. The better path: custody infrastructure with KYT built in from day one

Block at the source, right at the signing step. When transaction risk is assessed immediately before or during distributed signature generation (MPC threshold signing), the system can refuse to sign, and therefore refuse to let assets leave the wallet, the moment a receiving address falls into a risk category defined by the organization's own policy. This is in-line enforcement: risk control is not a side check running in parallel, it is an inseparable part of the transaction-processing flow itself. Unlike the add-on model, where a transaction is processed first and screened after, or held pending a response from an external service, the built-in model treats risk evaluation as a precondition for the transaction to exist at all, not a downstream audit step.

At a high level, the built-in flow looks like this:

Transaction request

|

v

Built-in KYT check ---> Automated policy engine

| |

(local scanning) (inline allow/block)

| |

v v

MPC threshold signing nodes

|

v

Pushed on-chain

Because the risk check sits inside the same loop as signing, rather than behind a separate API call, the three pain points from the add-on model are addressed by design, not bolted on:

- Lower external latency. No round trip to a distant third-party server. Scanning and signing happen in the same local loop, removing the cross-border network hop as a source of delay.

- Stronger data sovereignty. User PII and transaction metadata stay within the fintech's own private cloud or on-premise environment, aligned with the direction of data-residency expectations under frameworks like Indonesia's OJK rules or Vietnam's digital asset regulations. Whether a given deployment fully satisfies a specific regulator's requirements still depends on configuration, so this is a question to work through with legal counsel per market, not a property that follows automatically from architecture alone.

- More predictable infrastructure costs. Removing per-transaction third-party scanning fees means compliance cost does not scale linearly with volume the way an add-on model's billing does.

One infrastructure, one investment. Instead of maintaining two separate systems (custody plus a KYT add-on) with two cost lines, two operations teams, and a fragile integration layer in between, a single infrastructure solves asset custody and regulatory compliance at the same time, helping APAC fintechs approach international standards (EMEA/AMER) and expand cross-border without rebuilding every time regulation tightens. This is the same argument Fystack has made on the custody side more broadly: see why self-hosted MPC wallet infrastructure is becoming the standard heading into 2026 and a head-to-head comparison of self-hosted versus SaaS custody against Fireblocks. When an organization expands from one APAC market into another, say from Vietnam into Indonesia, where KYT is already a licensing prerequisite for institutional clients, having risk-monitoring built directly into custody makes the licensing process considerably faster, since there is no need to demonstrate how two separate systems coordinate.

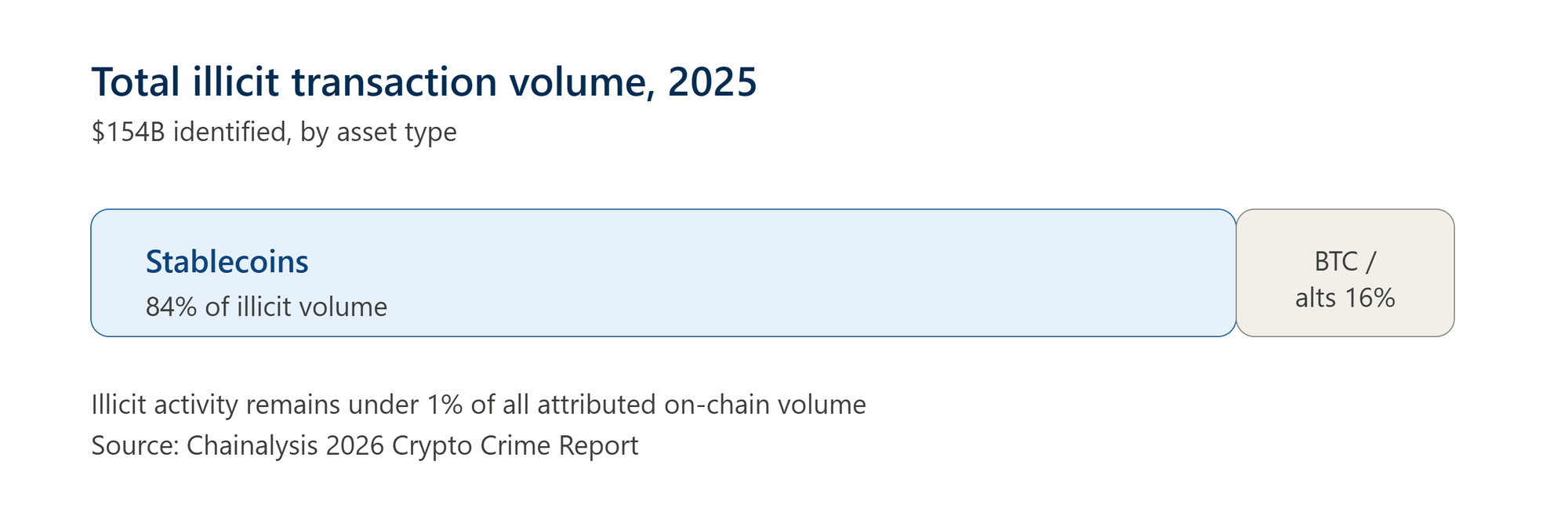

Here is roughly $154 billion in context: in 2025, illicit crypto addresses received at least that much in identified volume, and stablecoins accounted for 84% of all illicit transaction value, according to Chainalysis's 2026 Crypto Crime Report. That is not a reason to avoid stablecoins (legitimate stablecoin volume dwarfs illicit volume, and illicit activity remains under 1% of total attributed on-chain volume). It is a reason why the rails moving the most legitimate stablecoin volume are also the rails facing the most scrutiny, and why monitoring needs to be inseparable from the infrastructure processing that volume, not an afterthought attached to it.

Zoomed out, the difference between these two models is not just technical. It reflects two different philosophies of compliance: one treats it as an obligation to satisfy after the product is already live, the other treats it as part of the product's design from day one. In a region moving quickly from "gray zone" to codified law, the second approach is no longer a nice-to-have. It is becoming a condition for staying in the market at all.

How Fystack approaches this

Fystack builds self-hosted custody infrastructure with MPC at its core, combined with an automated policy engine and address-level risk analysis sitting directly at the transaction-signing layer, not as a separate risk-scanning service bolted on afterward. The withdrawal workflow is a concrete example: as described in how secure fund withdrawals work on Fystack, every outbound transaction passes through configurable approval thresholds and built-in risk verification before signing, not as an external check layered on top.

This approach is designed to let APAC fintechs solve both problems at once: operating custody securely, and meeting compliance standards that keep getting stricter, without having to trade off speed of deployment against depth of compliance.

If you are reassessing your organization's custody and compliance architecture, the Fystack team is glad to walk through the implementation in more detail.

FAQ

What is the difference between direct and indirect illicit exposure in crypto compliance?

Direct exposure means funds arrive immediately from a known illicit address, such as a sanctioned wallet. Indirect exposure means funds passed through one or more intermediary addresses first. Direct monitoring standards are fairly consistent worldwide; indirect monitoring is where regional and organizational practices diverge most, since there is no universal rule for how many hops back is "safe" to ignore.

Are stablecoins inherently risky because they dominate illicit transaction volume?

No. Stablecoins account for 84% of illicit transaction volume largely because they are also the dominant rail for legitimate cross-border payments, low volatility, and easy transferability. Chainalysis's own data shows illicit activity remains under 1% of total attributed on-chain volume. The takeaway is that monitoring needs to scale with where legitimate volume concentrates, not that the asset class itself is suspect

What is "add-on" KYT, and how is it different from a built-in model?

Add-on KYT means attaching a third-party transaction-monitoring service to an existing custody or wallet stack via API, separate from the signing process. It introduces integration risk between two independently evolving systems, latency while transactions wait on an external risk-scan response, and layered costs across licensing, per-transaction fees, and manual incident handling. In a built-in model, risk assessment happens at or before the signing step itself (for example, inside MPC threshold signing), so a policy engine can block a transaction from being signed at all if it matches a risk condition, rather than screening it after the fact.