Ethereum vs Solana: The Pros and Cons for Stablecoin Payments, Tokenization, and Enterprise Adoption

TL;DR

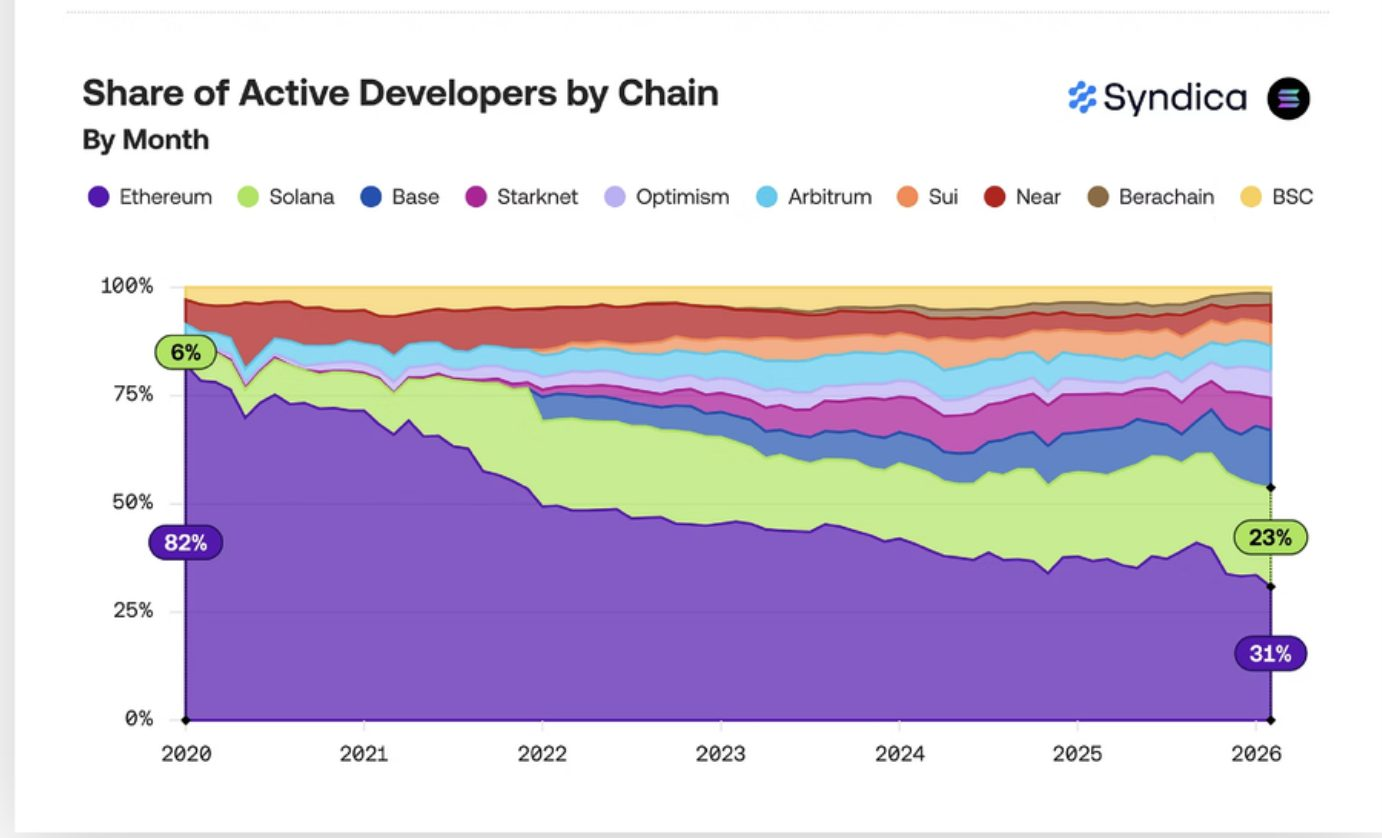

- Ethereum's developer share dropped from 82% to 31% since 2020 (Syndica, 2025). Solana now commands 23%. The competitive gap is real and closing fast.

- Despite losing retail users to faster chains, Ethereum settled $18.8 trillion in stablecoin volume and held over $99B in DeFi TVL in 2025, per DefiLlama - more than 9x the next largest Layer 1.

- JPMorgan launched its second tokenized money market fund on Ethereum in December 2025. BlackRock, Franklin Templeton, and Goldman Sachs followed with their own Ethereum-based products.

- The real question is not "Is Ethereum dying?" - it is "What kind of business are you building?" That answer determines the right chain.

- Businesses handling user funds on any chain face the same unsolved problem: key management at scale. Switching chains does not fix it.

If you have been following blockchain infrastructure in 2025, you have likely asked this: Is Ethereum still worth building on, or has it been left behind by faster, cheaper competitors?

The short answer is: it depends entirely on what you are building.

The longer answer is more useful for making an actual business decision. Ethereum is simultaneously losing ground in developer mindshare and retail user activity, while cementing itself as the default settlement layer for institutional capital. These two realities are not contradictions. They describe exactly who Ethereum is for in 2026.

The Numbers That Make Ethereum Look Weak

Let's not sugarcoat the challenge. The data against Ethereum is real.

According to a 2025 developer market report by Syndica, Ethereum's share of global active developers fell from 82% to 31% since 2020. Solana climbed from 6% to 23% in the same period. In 2025 alone, Solana onboarded 4,100 new developers versus Ethereum's 3,700 - the first time Solana led new developer signups.

User activity tells a similar story. Ethereum's weekly active user count fell below 3 million in 2025, while BNB Chain and Solana captured retail users with near-zero fees and sub-second confirmation times.

Solana's base layer regularly processes over 1,000 transactions per second with confirmation times near 0.4 seconds. Ethereum's L1 base layer still operates at roughly 15 to 30 TPS with 12-second block times.

These are not small gaps. For consumer-facing products requiring instant, cheap transactions, the performance difference is material.

So why are the largest financial institutions on the planet still choosing Ethereum?

The Numbers That Make Ethereum Look Irreplaceable

While retail users and new developers gravitate toward faster chains, institutional capital is flowing in the opposite direction.

According to the Ethereum Foundation's 2025 year-end summary - which aggregated data from DefiLlama, RWA.xyz, and Token Terminal - the network achieved the following in 2025:

- $99B+ in DeFi TVL, more than 9x the next largest Layer 1

- $18.8 trillion in stablecoin settlement volume

- $35B+ in ETH held across ETFs and institutional strategic reserves, per Ethereum Foundation summary

- $12B+ in on-chain real-world asset issuance

- Layer 2 fees below $0.01 per transaction, with combined L2 throughput exceeding 5,600 TPS

These figures reflect actual capital moving through Ethereum infrastructure in 2025. At the chain level for stablecoins specifically, DL News' State of DeFi 2025 report found that Ethereum maintained roughly 55% of total stablecoin supply, adding $50 billion in new issuance driven primarily by institutional flows and RWA infrastructure that prioritizes security and settlement guarantees.

What Institutions Actually Built on Ethereum. And Why That Matters

Why are major institutions still building on Ethereum instead of a faster chain?

When people say institutions are "building on Ethereum," they are usually not talking about speculative trading. They are building payment rails, tokenized funds, settlement infrastructure, and asset issuance systems. A few concrete examples illustrate the pattern.

- JPMorgan launched MONY (My OnChain Net Yield Fund) in December 2025 - its second tokenized money market fund on Ethereum, built via Kinexys Digital Assets. The fund enables programmable settlement, atomic subscription and redemption via stablecoins, and on-chain fund operations compliant with the Genius Act.

- BlackRock expanded its digital asset products tied to Ethereum-based liquidity ecosystems. BlackRock's digital asset AUM reached $78 billion by end of 2025, including an Ethereum ETP listed in the US. The BUIDL money market fund, launched on Ethereum in 2024, became the model for what institutional on-chain asset management looks like.

- Franklin Templeton brought tokenized fund products on-chain to support real-time transfer and programmable ownership - an operating model that requires deep stablecoin integration, not just a fast chain.

- Robinhood moved beyond exchange access and began developing Ethereum-compatible rails through its own Layer 2 architecture built on Arbitrum's Orbit stack, logging 4 million testnet transactions in its first week. The integration was designed to support tokenized stock trading, not just crypto-native activity.

These companies are not optimizing for the lowest transaction fee. They are optimizing for four things:

- Existing deep liquidity they can plug into immediately

- Compatibility with stablecoins, tokenized assets, and regulated DeFi protocols

- Audited infrastructure and mature tooling with years of production track record

- The ability to integrate with the broader financial stack - other institutions, compliant counterparties, and regulatory frameworks

That distinction matters for any business making a chain decision. Retail users choose chains based on speed and cost. Institutions choose based on where capital, compliance infrastructure, and counterparties already exist.

As CNBC reported in August 2025 on Ethereum's 10th anniversary: "Major institutions from BlackRock to Robinhood are building directly on Ethereum's rails, cementing its role as the backbone for stablecoins, tokenized stocks, and instant global payments."

Vitalik Buterin, in his January 1, 2026 message on CoinDesk, framed Ethereum's competitive advantage precisely: "Ethereum must prove itself as durable global infrastructure for an open internet." Not the fastest chain. The most durable one.

Ethereum's competitive advantage in 2026 is less about transaction throughput and more about acting as a coordination layer for financial infrastructure. That is a different product than Solana, and it serves a different customer.

Why Businesses Talk About Ethereum Like It Is Two Different Products

One reason conversations about Ethereum feel confusing is that people are often talking about two different things.

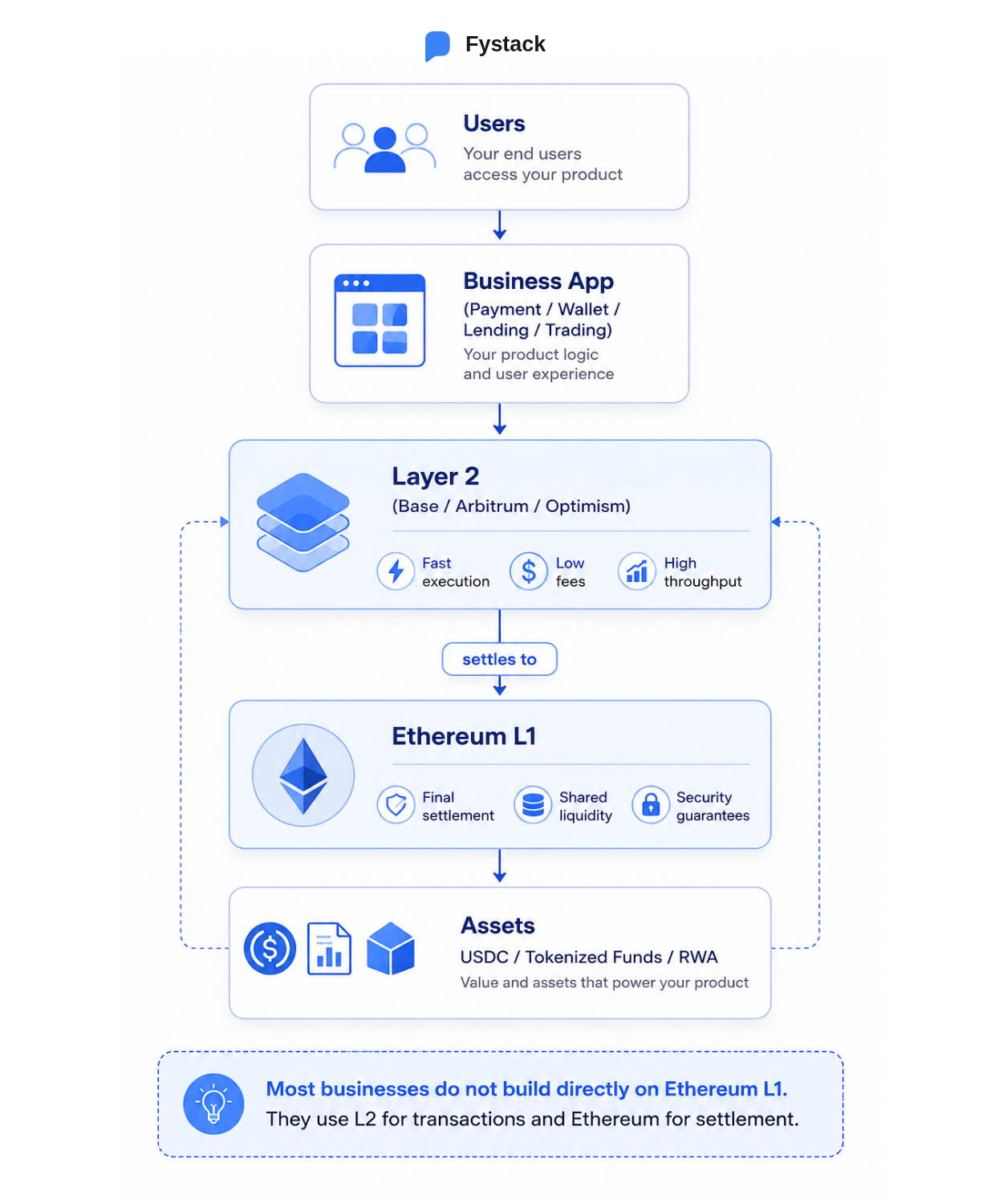

When critics say Ethereum is slow and expensive, they are usually talking about Ethereum L1 - the core network where transactions are ultimately finalized.

When companies say they are "building on Ethereum," they often mean Ethereum's broader ecosystem, especially Layer 2 networks like Arbitrum, Base, and Optimism.

A simple way to think about it:

- Ethereum L1 stores and secures value

- Ethereum L2 delivers the user experience

In practice, many businesses already use both.

A payment app might process thousands of low-cost transactions on Base, while relying on Ethereum underneath for settlement and asset security.

That changes the Ethereum conversation.

The question is no longer: Can Ethereum itself process every transaction?

The question becomes: Can the Ethereum ecosystem provide the speed users expect while keeping the liquidity, security, and interoperability businesses need?

For many teams in 2026, the answer has become yes.

That is why businesses increasingly treat Ethereum less as a single blockchain - and more as a financial operating system with different layers doing different jobs.

The Hidden Tradeoff of Ethereum L2s: Lower Costs, More Complexity

If I launch on Base, can my users instantly access liquidity on Arbitrum?

Not always.

Ethereum's Layer 2 ecosystem solved one major problem: transactions became dramatically faster and cheaper.

But it introduced another problem that businesses now have to manage: users, liquidity, and assets are spread across different networks.

In practice, that means a user holding USDC on Base cannot always use that balance immediately inside an app built on Arbitrum.

Moving funds between networks still requires extra steps, and depending on the route, users may wait minutes before funds arrive and pay additional fees along the way.

For products that depend on instant access to funds - payments, consumer wallets, trading, or remittance - that friction becomes a product decision, not just a technical detail.

The good news is that activity is increasingly concentrating instead of spreading everywhere.

By late 2025, most Ethereum L2 usage had consolidated around a small group of networks led by Base, Arbitrum, and Optimism. That reduces fragmentation compared to the early "launch another chain" phase and gives businesses clearer deployment choices.

At the same time, Ethereum's ecosystem is actively improving interoperability so users can move assets across L2s more seamlessly.

The direction is clear: over time, users should care less about which L2 they are on.

But that experience is not fully here yet.

For businesses building today, the practical lesson is simple:

L2s solve cost and scalability. They do not automatically solve liquidity and user experience.

Choosing an L2 is increasingly less about gas fees, and more about where your users, assets, and operational workflows already live.

What a Startup Actually Built on Base. And What It Proves

Can a small team realistically build on Ethereum L2 without BlackRock's resources?

Morpho is the clearest answer to this question.

Morpho is a permissionless lending protocol, not a bank, not a regulated institution, not a billion-dollar incumbent. It was built by a small team on a modular smart contract architecture deployed on Base. The design is relatively simple: isolated lending markets with a curator layer that allocates deposits across them.

In September 2025, Coinbase integrated Morpho into its consumer app to offer USDC lending to its 9.3 million monthly active users. Users could borrow against crypto collateral or earn up to 10.8% APY on stablecoins without the Morpho team being involved in the distribution at all.

The results, per multiple verified sources:

- Total USDC originations through the Coinbase integration exceeded $2.17 billion

- Morpho's TVL on Base grew 1,906% year-to-date in 2025, from $48.2M to $966.4M

- By April 2026, total Morpho TVL crossed $10 billion across deployments

- Apollo Global Management ($940B AUM) signed a cooperation agreement to acquire up to 90 million MORPHO tokens over 48 months

Morpho did not raise a massive round to achieve this. It built composable infrastructure on an L2 where distribution - via Coinbase's existing user base - could flow directly on-chain without any integration friction on Morpho's side.

This is the startup case for Ethereum L2 that the BlackRock examples do not capture: if your product is composable and your distribution partner already has Ethereum infrastructure, the network effects do the work. Morpho did not need to acquire users. It needed to be in the right ecosystem when Coinbase needed a lending primitive.

That dynamic is not available on chains without deep institutional and consumer distribution already embedded. It is the compounding advantage Ethereum's ecosystem has built over a decade.

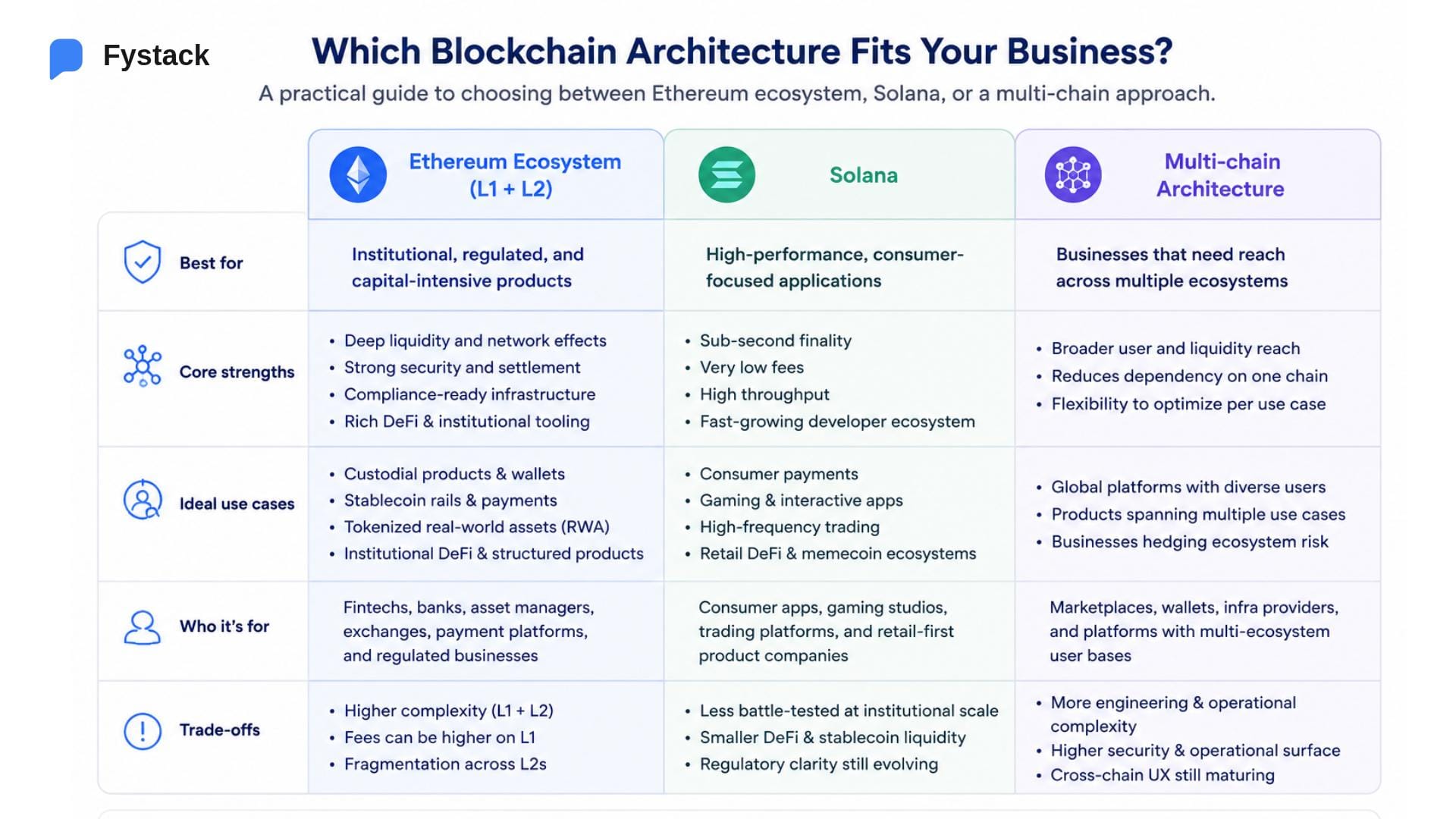

Ethereum vs. Solana in 2026: A More Honest Picture

Is Ethereum better than Solana for business in 2026?.

This is the wrong question. The right question is which chain fits your specific use case.

Solana has evolved well beyond its early reputation as the chain for gaming and micropayments. As Fystack's own analysis of Solana's recovery documented, Solana entered 2026 with a stablecoin market cap exceeding $15.5 billion and growing fintech infrastructure. The network has established itself in high-frequency DeFi, global payments, and increasingly in RWA activity.

Solana increasingly competes in payments and asset infrastructure, but still over-indexes toward high-throughput consumer experiences. That is not a weakness, it is a design choice with genuine strengths.

The more accurate comparison today looks like this:

The honest business case for Ethereum in 2026 is not that it is the best chain for every use case. It is that it is the best-suited chain for use cases where liquidity depth, institutional trust, compliance tooling, and settlement finality are non-negotiable.

What are the biggest security risks for businesses building on Ethereum or any chain?

Here is the part of chain selection conversations that almost never gets addressed: switching chains does not fix your biggest operational security exposure.

According to TRM Labs' January 2026 crypto crime report, infrastructure attacks targeting keys, wallets, and access-control systems drove the majority of crypto's $2.87 billion in 2025 hack losses - outpacing smart contract exploits. The attack surface is not the chain. It is the key management layer sitting on top of it.

This is the failure pattern that repeats across custodial businesses regardless of chain: teams invest heavily in smart contract audits, then leave key management as an afterthought. A hot wallet signing thousands of transactions per day is a single point of failure whether it lives on Ethereum, Solana, or any other network.

As Ethereum's L2 ecosystem expands, the key management problem compounds further. Managing signing keys across Ethereum L1, Arbitrum, Base, and Optimism simultaneously while maintaining compliance audit trails is a fundamentally different operational challenge than a single-chain deployment.

Businesses rarely fail because they chose the wrong chain. They fail because operational controls do not scale with adoption.

The controls that matter at scale are:

- Custody architecture: how keys are stored, rotated, and accessed

- MPC infrastructure: eliminating single points of failure through threshold signing

- Wallet orchestration: coordinating hot, warm, and cold fund movement securely

- Compliance tooling: maintaining audit trails that satisfy regulators and institutional partners

None of these are solved by selecting a faster L1.

Further reading on this topic from the Fystack team:

- Self-Hosted vs. SaaS MPC: Which Custody Model Fits Your Business? - a breakdown of the custody architecture decision that comes after chain selection.

- Fystack vs. Fireblocks: What Is the Future of Crypto Asset Custody? - how self-hosted MPC compares to managed SaaS at institutional scale.

- From Hot to Cold: Secure Fund Movement Architecture - the operational security layer that chain selection does not replace.

Chain Choice Is Only Half the Decision

Ethereum remains the default settlement layer for many institutional and regulated use cases. Faster chains continue to win where speed and cost matter most.

But the chain is rarely what breaks a business.

As products scale, the harder problems become operational: custody, signing flows, key management, compliance controls, and moving assets across ecosystems without adding risk.

That is where infrastructure matters.

Fystack helps businesses build and operate on-chain products without inheriting the operational complexity behind wallets, custody, and multi-chain execution.

Share what you are building: contact Fystack here

Follow on LinkedIn: Fystack

Frequently Asked Questions

Is Ethereum still too expensive for startups in 2025?

On L1, yes, fees remain relatively high for high-frequency transactions. But Ethereum L2 networks (Arbitrum, Base, Optimism) dropped fees below $0.01 per transaction in 2025 while settling on L1 security guarantees. For most startup use cases, deploying on an L2 makes Ethereum cost-competitive with faster chains.

Is Ethereum safer than Solana for business?

"Safer" depends on the layer you are comparing. Ethereum's base layer has the longest uninterrupted security track record and the most audited smart contract infrastructure. Solana has faced network stability issues historically, though its uptime improved significantly in 2024 and 2025. For both chains, the primary security risk for businesses is not the protocol layer, it is key management infrastructure, which sits above the chain entirely.

Can businesses migrate between chains later?

Technically yes, but the cost is high. Smart contracts must be redeployed, liquidity must be rebuilt, and user flows must be migrated. Chains also develop different tooling ecosystems over time. Businesses that anticipate multi-chain users are better served by designing chain-agnostic architecture early than retrofitting it after launch.

Should fintech companies use Ethereum L1 or L2?

For most fintech use cases - payments, stablecoin rails, custodial wallets - deploying on an Ethereum L2 is the practical choice. L1 is appropriate for high-value settlement finality and applications requiring maximum decentralization guarantees. Many production deployments use both: L2 for transaction execution, L1 for settlement anchoring.

Does multi-chain architecture increase security risk?

Yes, in most cases. Each additional chain integration adds a new key management surface, a new set of smart contract risks, and additional operational complexity. Multi-chain custody requires explicit architecture decisions about key isolation, cross-chain signing policies, and unified audit logging. Teams that adopt multi-chain without addressing these controls multiply their attack surface without a proportional increase in security coverage.

Is Ethereum the right blockchain for a fintech startup in 2026?

If your product involves stablecoin payments, asset tokenization, custodial wallets, or regulated DeFi - yes, the Ethereum ecosystem (L1 plus L2) remains the most mature and institutionally connected infrastructure available. If your product requires consumer-scale throughput at near-zero cost, evaluate both Ethereum L2s and high-performance alternatives like Solana before committing.